1. Introduction

The UK restaurant sector remains a cornerstone of the wider hospitality economy despite operating in a period characterised by economic uncertainty, inflationary pressures and changing consumer behaviours. Demand for eating out remains resilient, reflecting the enduring importance of restaurants as venues for social interaction, convenience, and leisure. While consumers remain committed to dining out and ordering takeaway food, their purchasing decisions have become increasingly value-driven. Customers are more selective about discretionary spending and are actively seeking promotions, meal deals, fixed-price menus and loyalty rewards that enhance perceived value.

2. Current trend in the market

Alongside these changes in consumer behaviour, the industry is undergoing a significant structural transformation. Digital technologies have moved from being optional enhancements to becoming core operational requirements. Online ordering, mobile applications, delivery platforms, digital payment systems and customer loyalty programmes have become essential components of the restaurant value proposition. Consumers increasingly expect seamless, convenient and personalised dining experiences across both physical and digital channels.

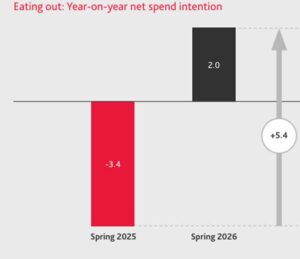

Figure 1: Eating out year-on-year net spending intentions; source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

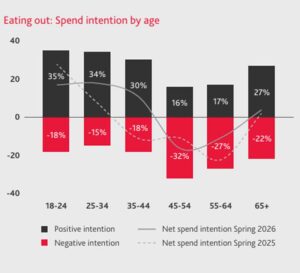

Figure 2: Eating out: Spend intention by age; Source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

Eating-out sentiment has strengthened considerably over the past year, reflecting a gradual improvement in consumer confidence and a renewed willingness to spend on out-of-home dining occasions. However, this recovery is not uniform across demographic groups. By 2026, the Office for National Statistics forecasts a 2.8% decline in the population of children aged 14 or younger, while expecting a 2.2% increase in the 15 to 29 age group and an impressive 7% increase in those aged 75 and older. According to Lumina Intelligence, based on their Eating and Drinking Out Panel data, older consumers are gradually returning to dining out, while those aged 25 to 34, the most active group in eating out, have shown a strong recovery. Additionally, younger consumers aged 18 to 34 remain the primary drivers of demand, with fairly robust spending intentions and frequent interactions with foodservice establishments. At the same time, the re-emergence of the 35–44 age cohort as active participants in the eating-out market represents a particularly positive development. As household financial pressures begin to ease and consumer confidence improves, this group is increasingly returning to restaurants for family gatherings, social occasions and shared experiences. Consequently, operators that can effectively cater to the preferences of both younger, experience-seeking diners and the family-oriented needs of the 35–44 demographic are likely to be best positioned to benefit from the ongoing market recovery. Such businesses will be able to capture demand across multiple customer segments, strengthening both customer retention and long-term revenue growth.

Figure 3: Trend for deliveries from restaurants; source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

Figure 3: Trend for deliveries from restaurants; source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

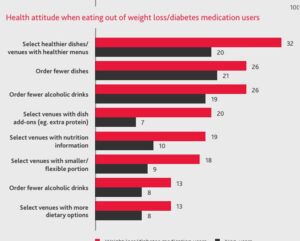

Figure 4: Consumers’ health consideration while eating out; Source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

Figure 4: Consumers’ health consideration while eating out; Source: LEIS-Report-Restaurant-and-Bars-Report-2026-March-2026.pdf

The two charts (Figure 3 and 4) reveal important shifts in consumer engagement with restaurants, highlighting both changing discovery behaviours and the growing influence of health-conscious consumption. First, delivery platforms are increasingly serving as channels for restaurant discovery. Among frequent delivery users, 42% have ordered food from a restaurant they had neither previously visited nor heard of, compared with 33% of all delivery users. This suggests that regular users of food delivery services are more willing to experiment with unfamiliar brands, indicating that digital platforms are becoming important mechanisms for customer acquisition and market expansion. For restaurant operators, online visibility, platform ratings and digital marketing are therefore becoming critical drivers of customer engagement and trial.

A second notable trend is the growing importance of health-oriented decision-making when dining out, particularly among consumers using weight-loss or diabetes medication. Compared with non-users, these consumers are significantly more likely to choose restaurants offering healthier menus, nutritional information, flexible portion sizes and dish modifications such as additional protein. They also tend to order fewer dishes and consume less alcohol when eating out. Collectively, these trends indicate that the future restaurant market will be shaped by two powerful forces: digital discovery and increasing demand for healthier, more personalised dining experiences. Restaurants that successfully combine strong digital engagement with health-conscious menu innovation are likely to enjoy a competitive advantage in attracting and retaining consumers.

The strong consumer demand has not translated into improved profitability. Rising labour costs, increasing National Insurance contributions, food inflation, energy prices and ongoing recruitment difficulties continue to place considerable pressure on operating margins. These challenges are particularly acute for small and independent operators with limited financial resilience. As a result, the sector has witnessed an increase in restaurant closures and insolvencies. In this environment, business success is increasingly determined by an operator’s ability to improve efficiency, embrace technology, differentiate its offering and respond effectively to evolving customer expectations. The following section delves into different types of restaurants and their specific areas of strengths and concerns.

3. Analysis of Key Restaurant Segments

Quick-Service Restaurants (QSRs)

Quick-service restaurants (QSRs), including fast-food chains and takeaways, are among the largest segments of the UK restaurant market, driven by consumer demand for affordability, convenience, and speed. The growth of delivery services and mobile ordering has bolstered this segment. However, QSR operators face challenges such as labour shortages and rising wage costs. Many rely on third-party delivery platforms, which can eat into profits. Additionally, competition from supermarkets and convenience stores offering ready-to-eat meals is increasing.

Despite these challenges, the outlook for QSRs is positive, with growth opportunities in digital innovation and operational efficiency. Mobile ordering, self-service kiosks, and digital payments enhance customer experience and reduce bottlenecks. Drive-through and click-and-collect models remain popular, while customer data allows for personalised marketing and loyalty programs that encourage repeat visits.

Casual Dining Restaurants

Casual dining restaurants, including family eateries and mid-market chains, face challenges in a competitive market, caught between budget quick-service and high-end dining. Many struggle to justify their prices as consumers seek value for money, compounded by rising operating costs and cheaper alternatives. To stand out, operators need to focus on experience-led differentiation. By offering flexible menus, value bundles, family packages, and themed events, they can enhance perceived value and foster customer loyalty. Those balancing affordability with unique experiences are likely to succeed in the current landscape.

Fine Dining and Premium Restaurants

The premium dining sector remains one of the most distinctive and resilient areas of the UK restaurant industry. Michelin-starred establishments, destination restaurants and chef-driven concepts continue to attract affluent consumers, business travellers and international visitors seeking exceptional food and service experiences.

Although premium consumers tend to be less sensitive to price increases, fine dining operators face their own set of challenges. The sector relies heavily on highly skilled culinary and front-of-house talent, making it particularly vulnerable to labour shortages and rising employment costs. Increasing ingredient, utility and procurement costs have also intensified pressure on financial performance. At the same time, customer expectations continue to rise. Diners now expect not only outstanding food and hospitality but also strong commitments to sustainability, ethical sourcing and environmental responsibility.

Future growth within the premium segment will be driven by experiential value rather than food quality alone. Consumers increasingly seek immersive experiences that combine gastronomy with storytelling, entertainment and cultural engagement. Chef-led branding and culinary narratives provide important opportunities for differentiation, allowing restaurants to build strong emotional connections with customers. Furthermore, growing interest in locally sourced, seasonal and sustainable ingredients enables premium operators to reinforce their authenticity, justify premium pricing and appeal to a growing segment of environmentally conscious consumers.

Independent and Ethnic Restaurants

Independent and ethnic restaurants play a vital role in the UK’s diverse foodservice sector, offering authentic dining experiences distinct from mainstream chains. However, they face challenges such as limited purchasing power and financial constraints, which hinder their competitiveness in negotiating supplier deals and investing in marketing and technology.

Despite these obstacles, these establishments enjoy unique advantages, as consumer demand for authenticity and cultural diversity is on the rise. Many diners seek distinctive experiences that reflect cultural traditions, and strong community ties can boost customer loyalty and word-of-mouth promotion. Additionally, niche cuisines allow for market differentiation that larger chains struggle to replicate.

Cloud Kitchens and Delivery-Only Concepts

Cloud kitchens, ghost kitchens and virtual restaurant brands represent one of the fastest-growing innovations within the restaurant industry. By operating without customer-facing dining spaces, these businesses significantly reduce occupancy and front-of-house costs, creating a leaner operating model focused entirely on online orders and delivery.

The model offers clear financial advantages but is not without risk. Dependence on delivery aggregators can reduce profitability and limit direct access to customers. In addition, the absence of face-to-face interaction presents challenges for building brand loyalty and emotional customer connections. Competition within digital marketplaces is also intense, making customer acquisition increasingly expensive.

Nevertheless, cloud kitchens offer substantial growth potential. Lower capital requirements reduce barriers to entry and allow operators to test new concepts with less financial risk. The model supports rapid menu innovation and enables businesses to respond quickly to emerging consumer trends. Perhaps most importantly, a single kitchen facility can support multiple virtual brands simultaneously, allowing operators to target diverse customer segments while maximising operational efficiency and asset utilisation.

4. Strategic Challenges Facing the Industry

The restaurant industry faces several structural challenges. Firstly, persistent cost inflation is squeezing margins due to rising food prices, labour costs, rent, and utilities, prompting operators to rethink pricing and supply chain strategies. Secondly, workforce issues like high turnover and skills shortages are impacting service quality and raising costs. Thirdly, consumer expectations for value, convenience, quality, sustainability, and memorable experiences are complicating business strategies. Lastly, technology has become essential, with customers expecting digital reservations, online ordering, mobile payments, and personalised loyalty programmes. Without investing in these areas, operators risk losing relevance.

5. Strategic Recommendations

To navigate these challenges successfully, restaurant operators should focus on six key priorities.

Develop experience-led propositions. Dining experiences must extend beyond the food itself. Themed events, storytelling, chef interactions and immersive concepts can strengthen customer engagement and support premium pricing.

Strengthen digital capabilities. Investment in online ordering platforms, customer relationship management systems, loyalty programmes and data analytics can improve customer retention and operational efficiency.

Enhance value perception. Rather than relying solely on discounting, restaurants should use fixed-price menus, meal bundles and loyalty rewards to demonstrate value while protecting profitability.

Diversify revenue streams. Businesses should explore complementary channels such as takeaway services, delivery, catering, food halls, pop-up operations and retail product extensions to reduce reliance on a single source of income.

Invest in workforce retention. Training, career development opportunities, employee wellbeing initiatives and flexible working arrangements can improve retention and service quality while reducing recruitment costs.

Embed sustainability into operations. Reducing food waste, sourcing locally where possible and promoting sustainable business practices can strengthen brand reputation and align with evolving consumer values.

6. Conclusion

The UK restaurant industry remains fundamentally robust, supported by strong consumer demand and a continuing appetite for dining experiences. However, the sector is undergoing significant transformation as economic pressures, technological change and evolving customer expectations reshape the competitive landscape. Long-term success will depend on operators’ ability to balance operational efficiency with innovation, deliver meaningful customer value without excessive discounting, and create distinctive experiences that foster loyalty. Businesses that successfully integrate digital capability, experiential differentiation, workforce development and sustainability into their operating models will be best positioned to achieve sustainable growth in an increasingly competitive market.

References:

- https://www.restroworks.com/blog/uk-restaurant-industry-statistics/

- https://www.bdo.co.uk/en-gb/insights/industries/leisure-and-hospitality/restaurant-and-bars-report

- https://store.mintel.com/report/uk-eating-out-review-market-report

- https://commonslibrary.parliament.uk/research-briefings/cbp-10333/

- https://www.restroworks.com/blog/uk-restaurant-industry-statistics/

- https://www.statista.com/topics/3131/restaurant-industry-in-the-united-kingdom-uk/#topicOverview

Dr Bidit L. Dey