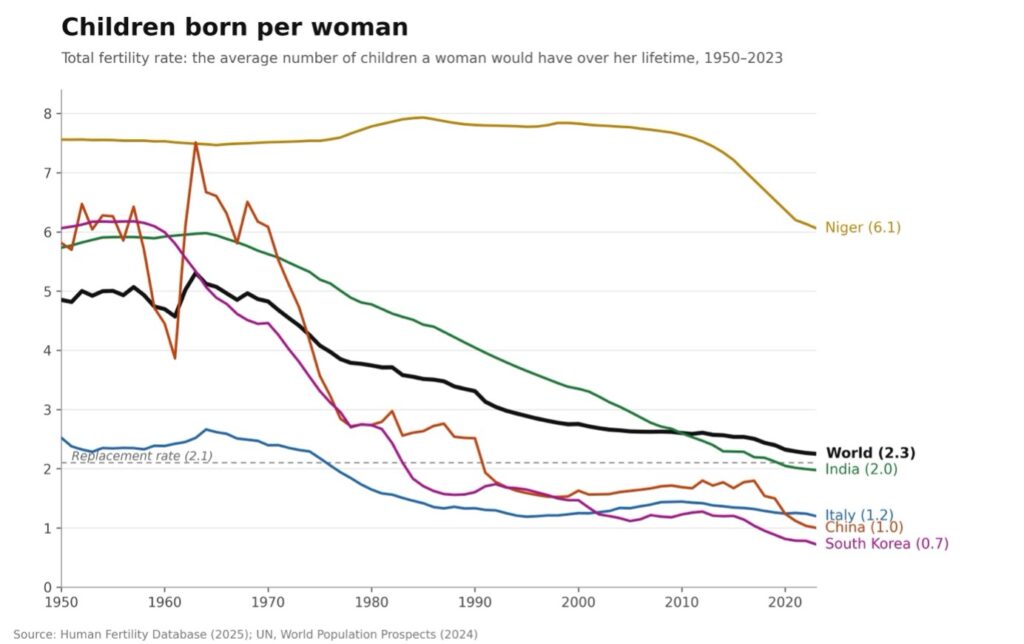

Governments across advanced and emerging economies have treated declining fertility as primarily a social-policy problem: reducing fertility has passed from being an outright policy goal to an enemy to beat. Family policy such as baby bonuses, parental leave expansions, childcare subsidies, and tax incentives are becoming more central in the policy debates, with the concurrent objective of raising fertility and promoting for gender equality. All around the world, fertility rates have continued to fall almost independently on the generosity of child-related welfare provisions. As of 2021, countries representing roughly 73% of the world’s population had fertility rates below the replacement level of 2.1 children per woman, compared with just 4.3% in 1960. World-wide fertility rate is now at 2.25,quite close to the replacement level of 2.1.

A growing body of economic research suggests that policymakers may be looking in the wrong place when tailoring family policies. Rather than tax breaks, bonuses or parental leave policies, it is housing the main channel to which one may try to increase fertility.

Across different countries, methodologies, and institutional settings, researchers are increasingly finding that access to affordable housing, homeownership opportunities, housing wealth, and mortgage financing play a central role in determining whether families have children—and when they do so. If governments want to address demographic decline, housing policy must become demographic policy.

Housing Is Not Just Another Consumer Good

Housing occupies a unique place in household finances. It is typically the largest asset a family owns and the largest financial commitment it makes. Housing determines access to schools, neighborhood quality, commuting patterns, and the amount of physical space available for raising children, yet fertility debates have often overlooked this.

A recent study (van Doornik et al., 2025) provides some of the strongest causal evidence to date. Exploiting randomized housing-credit lotteries in Brazil, the authors track more than 150,000 participants over nearly two decades. Among individuals aged 20–25, gaining early access to housing finance increases the probability of having children by 32% and increases the number of children by 33%.

More importantly, timing matters enormously. The authors estimate that completed lifetime fertility for a 20-year-old who gains immediate housing access is roughly twice as high as for someone who must wait until age 30 to obtain housing.

In other words, delayed housing access is not merely postponing births. It may permanently reduce the number of children people ultimately have. This finding directly challenges a common assumption in demographic policy (and journalistic narrative): that fertility delays can easily be reversed later in life and that demographic decline is just a statistical illusion create by parents postponing childbearing. Data suggests that biological constraints mean that many delayed births never occur.

Why Housing Affects Fertility

The Brazilian evidence also sheds light on the mechanisms involved. First, housing alleviates space constraints. Families living in overcrowded or poor-quality housing face both practical and psychological barriers to having children. The study finds larger fertility effects among households initially living in lower-quality and more congested housing.

Homeownership alsoimproves neighborhood quality. Lottery winners are more likely to relocate to areas with lower crime rates, higher incomes, and higher homeownership rates.

Finally, housing access appears especially important for lower-income households. Fertility responses are stronger among poorer families and among households where women account for a smaller share of household income, suggesting that financial constraints and the opportunity cost of child-rearing are central determinants of fertility especially in lower-income families.

These findings resonate with broader economic theory. One can think of households facing a “housing adequacy constraint”: families require a minimum amount of quality-adjusted housing per child. Relaxing that constraint directly increases the optimal number of children.

Housing Wealth Also Matters

Access to housing is only one side of the story. Housing wealth itself influences fertility decisions. In a landmark study of U.S. metropolitan areas, Dettling and Kearney (2014) found that rising house prices have sharply different effects on homeowners and renters. For homeowners, rising housing values increase home equity and ease financial constraints. For renters and prospective buyers, higher prices make family formation more expensive.

The authors estimate that a $10,000 increase in house prices raises fertility among homeowners by roughly 5%, while reducing fertility among non-homeowners by approximately 2.4%. At average U.S. ownership rates, the net effect remains positive.

The mechanism is intuitive. Rising home equity can function as a source of accessible wealth. Households may borrow against that equity or simply feel financially secure enough to undertake the substantial costs associated with child-rearing. Dettling and Kearney also calculate that housing costs represent the largest component of the cost of raising children.

This dual effect helps explain why fertility trends differ so sharply across demographic groups and housing-tenure categories.

Monetary Policy Has Demographic Consequences, too

The housing-fertility connection extends even further: into central banking. Research by Cumming and Dettling (2020) demonstrates that monetary policy affects fertility through mortgage markets. Using detailed UK data, the authors exploit variation in mortgage-rate exposure during the Great Recession. They find that a one-percentage-point reduction in policy rates increased birth rates by roughly 2% at the aggregate level and by about 5% among households directly exposed to lower mortgage payments.

Their estimates suggest that monetary easing generated approximately 14,500 additional births in the UK in 2009 and boosted birth rates by 7.5% over the following three years. The broader implication is that mortgage-market institutions matter. Countries with housing-finance systems that allow lower interest rates to pass quickly to households may experience stronger fertility responses than countries with more rigid mortgage structures.

It is now more common to promote a widening of the role of central bank from sheer price and financial stability into wider societal aims, such as the promotion of green transition and decarbonization. Nevertheless, fertility has not entered the policy debate as a potential further objective for monetary policy. This may soon change, as there is a wider acknowledgement of how demographic trends shape labor-force growth, long-run output, pension sustainability, and ultimately the equilibrium interest rate itself, making fertility be an overlooked transmission channel of monetary policy.

A New Policy Agenda?

This evidence is suggesting that governments should stop treating fertility policy and housing policy as separate domains. The evidence increasingly suggests they are deeply interconnected.

Housing supply constraints deserve greater attention. If younger households cannot access family-sized housing near employment centers, fertility will remain under pressure regardless of childcare subsidies or tax incentives.

Targeted housing-credit programs may also prove more effective than many conventional pronatalist policies. The Brazilian evidence suggests that accelerating housing access during peak childbearing years generates especially large fertility effects.

Finally, governments should evaluate demographic consequences when designing mortgage-market regulations, land-use rules, and housing-finance systems.

The Real Demographic Challenge

For years, debates about declining fertility have focused on cultural change, shifting preferences, and gender norms. Those factors undoubtedly matter. The recent evidence exposed in this article puts economics still matters. The emerging evidence from Brazil, the United States, and the United Kingdom points toward a common conclusion: when young adults can secure stable housing, fertility rises; when housing becomes inaccessible, fertility falls. Whether through housing credit, homeownership opportunities, housing wealth, or mortgage affordability, housing markets shape one of the most important decisions households ever make.

References:

- Cumming, F., & Dettling, L. J. (2020). Monetary Policy and Birth Rates: The Effect of Mortgage Rate Pass-Through on Fertility. Finance and Economics Discussion Series 2020-002, Board of Governors of the Federal Reserve System.

- Dettling, L. J., & Kearney, M. S. (2014). House Prices and Birth Rates: The Impact of the Real Estate Market on the Decision to Have a Baby. Journal of Public Economics, 110, 82–100.

- van Doornik, B., Fazio, D., Ramadorai, T., & Skrastiņš, J. (2025). Housing and Fertility. Working Paper, Imperial College London, National University of Singapore, Banco Central do Brasil, and Washington University in St. Louis.

Emanuele Bracco