Global Economic Rollercoaster: US Inflation Jitters, EU Green Surge, and China’s Tech Rebound 🎢

The VortexWeekly Economic and Financial News (Oct 5 – 11, 2025)

Summary: The first full week of October 2025 saw a whirlwind of economic activity. The US grappled with persistent inflation concerns despite strong jobs data, keeping the Fed on high alert. Europe, meanwhile, celebrated robust growth in its green energy sector, signaling a successful transition. China’s tech giants showed signs of a strong recovery, buoyed by domestic consumption and strategic policy shifts. Dive into the biggest headlines from around the globe!

United States: Inflation’s Stubborn Grip and the Fed’s Dilemma 🇺🇸

The economic spotlight in the US this week remained firmly on inflation. Fresh consumer price index (CPI) data released on October 8th showed a stubbornly high annual inflation rate of 4.2%. This figure, while a slight dip from last month’s 4.3%, still sits well above the Federal Reserve’s target. Core inflation, which excludes volatile food and energy prices, also remained elevated at 3.8%. This persistence sparked renewed debate about the timing and magnitude of future interest rate adjustments.

Despite inflation worries, the labor market continued its impressive run. The September jobs report, released on October 4th, revealed an addition of 210,000 non-farm payrolls, beating analyst expectations. The unemployment rate held steady at a healthy 3.7%. This dual narrative – strong employment but persistent inflation – presents a complex challenge for the Federal Reserve. Analysts now widely expect another interest rate hike by year-end, potentially pushing the federal funds rate above 5.5%. The housing market, in particular, has started feeling the pinch of higher borrowing costs, with new home sales declining for the second consecutive month.

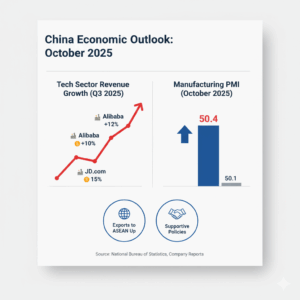

Key economic indicators for China in October 2025, highlighting tech sector growth and manufacturing activity.

European Union: Green Energy Powers Ahead 🌍⚡

The European Union delivered a refreshing narrative this week, showcasing remarkable progress in its green energy transition. A new report from Eurostat, released on October 9th, highlighted a 15% year-on-year increase in renewable energy production across the bloc. Solar ☀️ and wind 🌬️ power installations spearheaded this growth, contributing significantly to the EU’s energy mix. This surge directly impacts economic activity, creating thousands of new jobs in manufacturing, installation, and maintenance sectors.

Investment in sustainable technologies also saw a substantial boost. Several major EU countries announced new funding initiatives and private-public partnerships aimed at expanding charging infrastructure for electric vehicles and developing advanced battery technologies. The European Central Bank (ECB) maintained its cautious stance on interest rates, signaling that recent inflationary pressures appear to be moderating. Preliminary Q3 GDP estimates, while not fully released, suggest steady but moderate growth for the Eurozone, largely supported by robust domestic demand and export performance in niche high-tech sectors. The optimism surrounding the green transition provides a crucial counter-narrative to global economic uncertainties.

China: Tech Sector Rebounds Strong 💪🇨🇳

China’s economy showed signs of renewed vigor, particularly within its critical technology sector. Following a period of regulatory adjustments and global headwinds, major Chinese tech giants reported stronger-than-expected Q3 earnings this week. Alibaba, Tencent, and JD.com all posted healthy revenue growth, driven by a rebound in domestic consumer spending and strategic international expansion. The government’s recent supportive policies for the digital economy seem to be paying dividends, fostering innovation and market confidence.

Manufacturing data, released by the National Bureau of Statistics on October 7th, indicated a slight expansion in the Purchasing Managers’ Index (PMI) to 50.4, up from 50.1 last month. This suggests sustained activity in the industrial sector. Exports also remained robust, particularly to ASEAN nations and emerging markets, diversifying China’s trade relationships amidst ongoing geopolitical complexities. While real estate sector concerns persist, targeted government measures appear to be preventing a broader systemic risk. The People’s Bank of China (PBOC) signaled a willingness to use further targeted liquidity injections if needed to support economic stability, but maintained its primary focus on fostering high-quality growth.

Key economic indicators for China in October 2025, highlighting tech sector growth and manufacturing activity.

Global Market Reactions and Outlook 🌐

The divergent economic narratives from the US, EU, and China led to mixed reactions in global markets this week. US equities saw some volatility as investors digested inflation data and anticipated further Fed action. Technology stocks, however, showed resilience, benefiting from the robust performance of their Chinese counterparts and continued innovation. European markets generally maintained positive momentum, particularly those companies heavily involved in the renewable energy sector. Asian markets, especially in China, experienced a bullish sentiment driven by the tech rebound and stable manufacturing figures.

Commodity markets presented a varied picture. Oil prices saw a slight increase due to stable global demand forecasts, while industrial metals experienced moderate gains, reflecting the manufacturing activity in Asia. Gold, often seen as a hedge against inflation, saw minor fluctuations. Looking ahead, analysts will closely monitor central bank communications, particularly from the Federal Reserve, for clearer signals on monetary policy. Geopolitical developments and their potential impact on supply chains also remain a key area of focus for the global economy. The interplay between inflation, interest rates, and sector-specific growth will continue to shape market dynamics in the coming weeks.

Conclusion: A Tiptoe Towards Stability? 🤔

The week of October 5th-11th, 2025, underscored the complex and interconnected nature of the global economy. While the US grapples with persistent inflationary pressures, the EU’s green transition offers a blueprint for sustainable growth, and China’s tech sector signals a robust domestic recovery. Each region faces unique challenges and opportunities, contributing to a global economic landscape that is constantly shifting. Investors and policymakers alike will need to remain agile, adapting to emerging trends and navigating potential headwinds. The journey towards a stable and prosperous global economy continues, with key decisions and market shifts awaiting us.