Abstract: Recent geopolitical tensions and disruptions in global energy markets have

renewed attention on how monetary policy should respond to supply-driven inflation. The

standard prescription is to “look through” temporary energy shocks, as tightening

monetary policy would disproportionately hurt poorer households already affected by

rising prices of essential goods. However, a stronger policy response becomes necessary

when these shocks feed into core inflation or when inflation expectations begin to rise

persistently (i.e. become “de-anchored”).

The triggered by the US-Israeli beheading of the Iranian leadership on February 28th are yet

another hit to the world energy market. In this age of geopolitical fragmentation energy

shocks are becoming more and more frequent.

A disruption of the strait of Hormuz—through which roughly a fifth of global oil supply

transits—is going to unfailingly hit headline inflation and it will transmit rapidly into

production costs, labour demand, and ultimately household welfare. For central banks, the

familiar question would return with urgency: is inflation temporary or is it there to stay?

should central banks “look through” the resulting spike in energy prices just waiting for this

single wave to pass, or should they instead lean against the inflationary tide with restrictive

monetary policy? What recent research makes clear is that this is no longer a simple trade-off

between inflation and output, or between temporary and permanent shocks. When energy is a

necessity and unemployment risk is imperfectly insured, supply disruptions of this kind

reshape the distribution of economic pain—turning what appears to be a price stability

problem into a labour market, inequality and welfare problem.

Energy shocks generate a supply-driven inflation, i.e. an inflation surge triggered by the

increased production costs. The incidence of this surge is deeply unequal across society, with

poorer household taking the brunt of the hit, as a larger share of their expenditure is devoted

to essential items such as food and energy. The standard central-bank playbook is simple:

look through temporary energy shocks and focus on core inflation, but this fails to encompass

the heterogenous effect of shocks along the income distribution. Recent evidence and theory

suggest that this framework may be incomplete.

A recent paper in the Journal of Monetary Economics by ECB-economist Nicola Gnocato

(Gnocato, 2025), argues that energy shocks cannot be seen as mere (relative) price

disturbances. They interact with labour market risk and household heterogeneity in ways that

challenge the basic view of optimal monetary policy. His insight forces a reconsideration of

how aggressively central banks should respond to core inflation in the wake of energy

shocks.

Energy shock are not hitting everyone in the same way

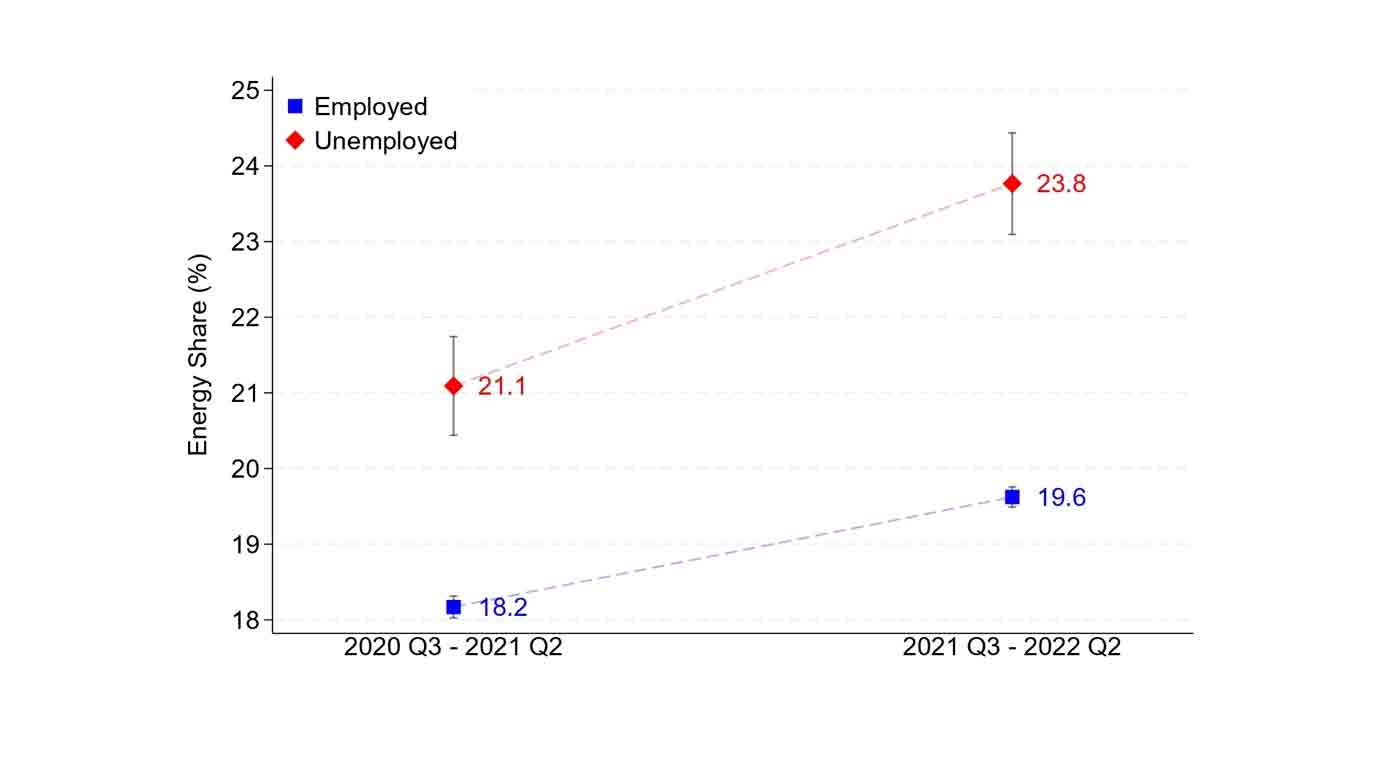

The starting point is empirical. Microdata from the ECB’s Consumer Expectations Survey

(ECB-CES) show that unemployed workers not only reduce total consumption but also

allocate a larger share of expenditure to energy-intensive goods such as utilities. This is not

surprising: energy is a necessity.

Figure 1. Energy Shares of the Employed and the Unemployed (from Gnocato,

2025).

Notes: The figure reports the average shares of energy-intensive consumption expenditure over time for

Notes: The figure reports the average shares of energy-intensive consumption expenditure over time for

employed and unemployed individuals interviewed in the ECB-CES survey.

Gnocato (2025) embeds this evidence in a tractable theoretical model which encompasses

labour market frictions and imperfections (technically speaking, a heterogenous-agent new-

Keynesian model with search and matching frictions and non-homothetic preferences). The

key mechanism is straightforward: unemployment both reduces income and increases

exposure to energy prices. Because energy consumption has a subsistence component, the

unemployed devote a larger share of their (lower) consumption to energy. At the same time,

energy is a complementary input in production, so higher energy prices reduce labour

demand and increase the likelihood of unemployment.

This interaction creates a feedback loop: energy shocks increase unemployment, which in

turn amplifies the welfare cost of those shocks. In equilibrium, the distribution of exposure to

energy prices becomes endogenous to labour market outcomes and hits more strongly the

lower-income household even more than expected.

In this environment, monetary policy faces a genuine trade-off. Stabilizing

inflation—specifically non-energy (core) inflation—requires tightening, which also increases

unemployment, pushing more and more households into the high-exposure state,

exacerbating the welfare costs of the shock.

Formally, the model generates an endogenous wedge between “natural” unemployment

(consistent with stable inflation) and “constrained-efficient” unemployment (welfare-

maximizing).

The optimal policy response is therefore neither strict inflation targeting nor full employment

stabilization. Instead, it involves partially accommodating a rise in core inflation to limit the

increase in unemployment. Maintaining employment shields workers from greater exposure

to rising energy prices.

Quantitatively, the model shows that fully stabilizing core inflation leads to excessive

unemployment, while fully stabilizing unemployment leads to too high inflation. The optimal

policy lies in between: a “mild reaction” to core inflation combined with full “look-through”

of the energy component.

What are central banks doing?

Interestingly, this prescription aligns with empirical evidence on central bank behaviour. A

report from the Bank of International Settlements (BIS, 2025) documents that advanced

economy central banks have typically responded to core inflation while “essentially

ignor[ing] changes in energy and food prices,” consistent with a look-through approach.

This approach is grounded in two classic considerations. First, monetary policy operates with

lags, so reacting to transitory commodity price shocks may be counterproductive. Second,

supply-driven shocks are stagflationary (i.e. they nudge the economy towards a high-inflation

high-unemployment state), creating a trade-off between inflation and output stabilization. In

such cases, a muted response to the energy component of the price-shock is often optimal.

However, the BIS also highlights that the environment may be changing. Commodity price

shocks are becoming larger, more frequent, more persistent and more disruptive, driven by

geopolitical fragmentation, climate change, and the energy transition. These developments

increase the risk of transitioning to a high-inflation regime and may limit the scope for central

banks to look through such shocks.

The Limits of “Looking Through”

The ECB’s recent strategy assessment provides further nuance (ECB, 2025). The “medium-

term orientation” of monetary policy explicitly allows policymakers to look through

temporary supply shocks to avoid unnecessary volatility in activity and employment. The

ECB also emphasizes the limits of this approach. Persistent or large shocks risk de-anchoring

inflation expectations, requiring a more forceful response. Large, sustained deviations can

destabilise longer-term inflation expectations, necessitating more aggressive monetary

tightening, but this may end up decreasing disproportionately poorer households’ welfare.

The emerging picture is one of competing forces. Heterogeneity and labour market frictions

amplify the welfare cost of unemployment, strengthening the case for a less aggressive

monetary policy reponse to energy shocks. On the other hand, structural changes—such as

more persistent shocks and the risk of de-anchoring—strengthen the case for tighter policy.

The policy problem is therefore what economist call “state-dependent”, i.e. it must depends

on other factors other than the simple size of the energy shock. When inflation expectations

are well anchored and shocks are perceived as transitory, the Gnocato (2025) logic

dominates: accommodating some inflation can improve welfare by limiting unemployment

and protecting vulnerable households. When expectations are at risk of de-anchoring, the BIS

and ECB concerns become paramount: failing to respond forcefully may lead to larger and

more persistent inflation, ultimately requiring even more costly tightening.

Policy Implications

What does this imply for central banks? First, the distinction between headline and core

inflation remains essential. Both the Gnocato model and empirical evidence support fully

looking through the energy component, which is largely exogenous and does not directly

affect domestic production decisions.

Second, the response to core inflation should be calibrated to labour market conditions and

distributional considerations. A mechanical rule reacting aggressively to core inflation may

be suboptimal when unemployment risk is high and heterogeneity is significant.

Third, communication becomes more challenging. The traditional narrative—ignore energy

shocks and focus on core—must be supplemented with an explanation of why some

accommodation of core inflation may be desirable in certain states of the world.

Finally, monetary policy cannot bear the entire burden. As the ECB notes, fiscal policy is

better suited to address distributional effects directly. Targeted transfers to vulnerable

households can mitigate the need for monetary accommodation, allowing central banks to

focus more squarely on price stability.

References:

- BIS (Bank of International Settlement) (2025). Commodity prices and monetary policy: Old

and new challenges (BIS Bulletin No. 96). Edited by: Avalos, F., Banerjee, R., Burgert, M.,

Hofmann, B., Manea, C., & Rottner, M. - ECB (European Central Bank). (2025). Report on monetary policy tools, strategy and

communication (Occasional Paper Series No. 372). European Central Bank. - Gnocato, N. (2025). Energy price shocks, unemployment, and monetary policy. Journal of

Monetary Economics, 151, 103734. https://doi.org/10.1016/j.jmoneco.2025.103734

Emanuele Bracco