US Credit Jitters, Bank Tax Shock & China’s Mixed Signals

The Vortex – Global Market Weekly – 3–9 July, 2025

The first week of August brought drama in markets worldwide. A U.S. credit rating scare and weak jobs data fueled hopes for Fed rate cuts – lifting Wall Street to record highs – while Europe weathered an Italian bank tax shock and the Bank of England cut rates amid cooling inflation. In Asia, Chinese stocks surged on stimulus bets despite deflation warnings, contrasting with Japan’s steadier outlook.

United States – Stocks Rebound as Fed Hints at Easing After Credit Scare

Wall Street roared back this week after enduring a credit rating jolt and signs of a cooling economy. Late in the prior week, Fitch Ratings unexpectedly downgraded U.S. sovereign debt from AAA to AA+, citing rising fiscal deficits and political turmoil. It was the first U.S. rating cut by a major agency in over a decade, and it initially spooked markets. The timing coincided with a disappointing July jobs report – employers added just 73,000 jobs in July, the weakest payroll gain since 2020[1]. Unemployment ticked up to 4.2%, reinforcing the view that the once-hot labor market is losing steam.

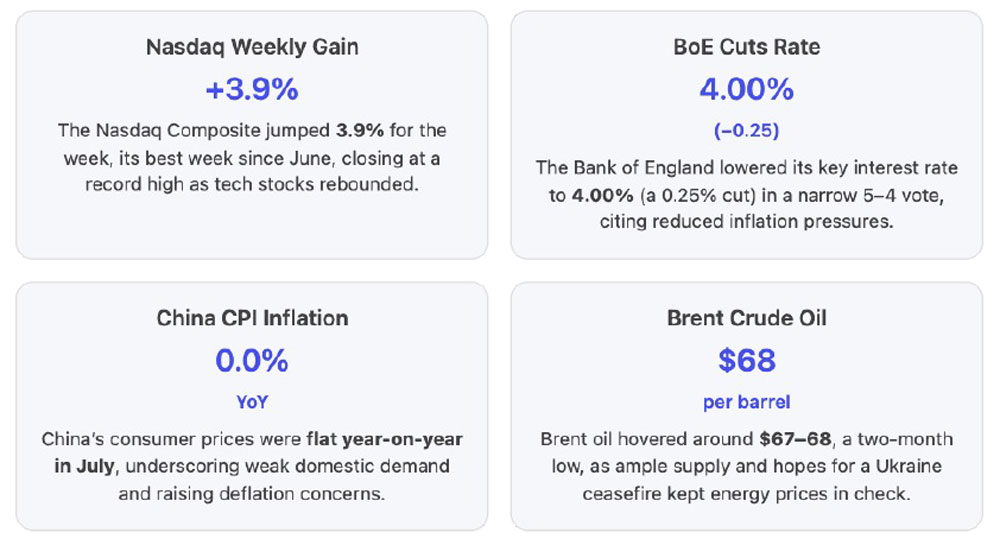

Faced with these headwinds, Federal Reserve officials quickly signaled a dovish shift. Fed Chair Jerome Powell (speaking a week later at Jackson Hole) and Governor Christopher Waller both hinted that rate cuts could be on the horizon, given that inflation has eased and job growth is faltering. Waller even commented that the Fed “should have cut in July” and urged colleagues to “get on with” a 0.25% cut in September[2][2]. Markets cheered this prospect of the Fed’s first rate reduction of 2025. Expectations for a September cut surged to ~80% odds. In turn, stocks staged a powerful rally: the S\&P 500 jumped +2.4% for the week and the Nasdaq Composite soared +3.9%, its best week since June[3]. Both indices closed at fresh record highs, fully erasing the prior week’s losses. The blue-chip Dow rose about +1.6%, putting it within 2% of its all-time peak[3].

Investors piled back into technology and growth stocks, which benefit from lower interest rates. Mega-cap tech leaders led the charge. Apple’s stock surged over 4% on Friday – capping a three-day, +13% run[3] – after the company announced a $100 billion U.S. manufacturing investment that won it exemptions from new chip tariffs. Alphabet and Tesla rose ~3% apiece on the week. Even embattled chipmakers rebounded: Nvidia gained 1% after recent dips, as reports hinted the U.S. might soften certain China export curbs[3]. In a sign of risk-on sentiment’s return, Bitcoin briefly hit a record $124,000 mid-week before settling around $117K[3], and gold prices spiked to an all-time high of $3,535/oz on safe-haven flows[3]. (Gold later eased to ~$3,460 as the White House clarified it wouldn’t impose new bullion tariffs[3].) Meanwhile, the U.S. 10-year Treasury yield, which had plunged to a three-month low ~4.18% during the height of the scare[3], climbed back up to 4.29% by Friday[3] as risk appetite returned.

Political and policy developments added both uncertainty and optimism. President Donald Trump continued his unorthodox interventions: after expressing “shock” at July’s weak jobs report, he fired the head of the Bureau of Labor Statistics, claiming the data was “rigged”[2]. This unprecedented move raised concerns about data integrity, though economists defended the reliability of the statistics[1]. On trade, the U.S. forged ahead with a wave of new import tariffs on dozens of countries (tariffs of 15–25% on goods from Europe, Asia, and beyond). These had been threatened for months and finally took effect August 1 after multiple delays[3]. However, fears of an escalating trade war eased slightly as there were no additional surprises beyond what was telegraphed. In fact, U.S. and China trade negotiators were in talks to extend a current tariff truce set to expire Aug. 12[3]. The mere possibility of avoiding a fresh U.S.-China tariff spike helped buoy sentiment. All told, by week’s end investors seemed to look past the credit downgrade and trade drama, focusing instead on the growing likelihood that the Fed will ease monetary policy to keep the expansion on track. With inflation down to ~2.7% and 10-year yields stabilizing, the ingredients are falling into place for a potential “Goldilocks” scenario of lower rates and sustained growth – the catalyst of this week’s market euphoria.

European Union – Italy’s Bank Tax Stunner, BoE Eases Rates as Inflation Cools

European markets experienced a roller coaster week, swinging from relief over cooling inflation to shock over an Italian banking tax. Early in the week, data showed the eurozone economy barely avoided recession in Q2. An initial estimate put Eurozone GDP growth at a meek +0.1% quarter-on-quarter[4], but at least it was positive. Spain grew a solid 0.7%, offsetting small contractions in Germany and Italy[4]. Meanwhile, eurozone inflation continued to ease. In July, France’s annual CPI fell to just 0.8% – its lowest in years – while Germany’s ticked up slightly to 2.1%[2][5]. The bloc’s overall inflation is now in the mid-2% range, down sharply from 5–6% at the start of the year. This improving backdrop set a calm tone at first. EU-U.S. trade relations also improved: negotiators in Washington and Brussels signaled progress toward a deal that would avert harsh U.S. tariffs on European cars and pharmaceuticals. The prospect of a trade truce (after months of tension) buoyed European industrial and auto stocks modestly.

The calm was shattered on Tuesday when Italy’s government unexpectedly announced a 40% windfall tax on bank profits. The one-time levy targeted banks’ extra profits from higher interest rates. The news sent Italian bank stocks into freefall: shares of giants like UniCredit and Intesa Sanpaolo plunged 8–10% intraday, and Italy’s FTSE MIB stock index tumbled over 2.5%. The sell-off quickly spread across Europe – bank indices in Spain, France, and Germany fell ~3%, dragging the pan-European STOXX 600 down 1.4% on the day. Analysts slammed the move as “retroactive interference” and warned it could backfire by tightening credit. Facing the market backlash, Rome scrambled to dial back the plan within 24 hours. By Wednesday, the Italian Economy Ministry issued an urgent clarification, capping the tax at 0.1% of a bank’s risk-weighted assets. This cap dramatically limited the tax cost (to about €2–3 billion total, vs. an initially feared €20B+). The partial U-turn sparked a sharp rebound in bank shares. Italian banking giants clawed back most of their losses by Thursday, and European stocks at large recovered. Still, the episode injected a note of caution. It highlighted the political risks in Europe’s financial sector, especially in countries like Italy where populist measures can emerge suddenly. Some investors may demand higher risk premiums for Italian assets going forward, given what one economist called a “major unforced error” by Rome.

Amid this drama, the Bank of England delivered a pivotal rate decision. On Aug. 7, the BoE’s Monetary Policy Committee cut the benchmark interest rate by 0.25% to 4.00%, resuming an easing cycle after a pause[2]. The vote was a close 5–4 split, reflecting debate among policymakers[2]. BoE Governor Andrew Bailey noted the decision was a “finely balanced” call between still-high inflation and a softening economy[2][2]. UK inflation, while down from double digits, remains sticky at ~3.8% (headline CPI) with core price growth above target. June’s CPI actually picked up to 3.6% from 3.4% in May[2], a surprise, which gave pause to some hawks. However, evidence of a cooling job market and stagnating growth tipped the scales. UK unemployment has crept up to 4.3%, and GDP shrank –0.1% in Q2[2][2]. These factors convinced the majority that a modest cut was prudent. The BoE emphasized it will be “gradual and careful” with further easing[2]. Notably, this was the BoE’s fifth consecutive quarterly rate cut, as it had already eased from 5.00% to 4.25% over the past year amid signs that Britain’s inflation surge had peaked. The policy pivot helped lift UK interest-rate-sensitive stocks; homebuilder shares rose and the FTSE 250 index gained ground. The British pound initially rose on the news (to ~$1.34[2]) but then slipped by week’s end as traders anticipate more cuts ahead.

Overall, European markets ended the week mixed but resilient. The STOXX 600 index recovered to finish roughly flat. Italy’s bank index ended down about 1% on the week – bruised but not broken. Germany’s DAX and France’s CAC 40 were little changed. London’s FTSE 100 outperformed slightly (+0.8%), aided by global commodity stocks and a weaker pound. European bond yields were stable; Germany’s 10-year Bund yield held around 2.60%, and Italy’s 10-year BTP yield hovered near 4.15%, up only modestly from before the bank-tax saga. In the energy market, oil’s decline was a tailwind for Europe’s inflation outlook: Brent crude at $67-68 is a boon for EU consumers and businesses, effectively lowering fuel costs. European natural gas prices also remained low thanks to ample storage, in stark contrast to the spikes of last summer. With recession fears easing and inflation cooling, the European Central Bank is now expected to pause rate moves in September. Barring new shocks, Europe appears to be entering a period of steadier, if sluggish, growth. The big question mark is whether policymakers can avoid “own goals” like Italy’s episode as they navigate this delicate recovery.

Asia – China’s Stock Frenzy vs. Economic Gloom; Japan Steady

Asian markets were led by a paradoxical China, where stock investors turned euphoric even as economic data showed deterioration. China’s economy sent more warning signs that its rebound is faltering. The most worrying: consumer prices in July were flat (0.0%) year-on-year[4], missing expectations of slight inflation and down from +0.1% in June. Effectively, China is teetering on deflation – a symptom of weak domestic demand. Producer prices fell 3.6% YoY, their 10th straight month of decline[4], reflecting overcapacity and commodity price drops. The property sector remains a drag; real estate investment has plunged ~12% this year, and new home prices keep slipping. In a sign of stress, Country Garden, one of China’s largest developers, was reported to miss interest payments on its debt this week (raising fears of default), though it has a 30-day grace period to resolve the issue. On the bright side, China’s trade data surprised to the upside. Exports in July rose +7.2% YoY[3], defying predictions of a slowdown. This was likely boosted by companies rushing out shipments before a potential reinstatement of tariffs (the U.S.–China tariff truce expires Aug 12). Imports also climbed 4.1%, the first annual increase in 2025 and the largest since early 2024[3]. These import gains hint at slightly better domestic demand for commodities and goods, or possibly stockpiling at lower prices. Despite the trade uptick, most economists caution that China’s underlying picture is weak – evidenced by falling factory prices and an official manufacturing PMI of 49.3 (contraction) in July[3].

Yet Chinese equity markets were on fire. Investors are betting that Beijing will unleash major stimulus to turn the tide. The benchmark CSI 300 index in Shanghai and Shenzhen jumped about +3% for the week (now +10% for August so far), reaching its highest level in nearly a decade. The broader Shanghai Composite climbed for an eighth straight session, a streak not seen since 2015. Trading volumes have exploded and margin debt has surged – margin financing on A-shares hit ¥2.0 trillion by Aug 5, the first time above that level since 2015’s speculative boom[5]. This suggests Chinese retail traders are leveraging up, eager not to miss the rally. The government has been sending pro-market signals: state media have run commentaries urging investors to “buy the dip,” regulators eased some share trading rules, and there are rumors of an imminent cut to bank reserve requirements or interest rates. Thus, even with bad economic news, the market’s logic is “weak data = more stimulus.” It’s a risky dynamic (veterans recall the 2015 bubble-and-crash), but for now the momentum is powerful. Hong Kong’s Hang Seng index also rose ~1.5%, lifted by big Chinese tech names and hopes that U.S.–China tensions won’t worsen. One concrete positive on that front: Beijing and Washington reportedly made headway on trade talks, with China agreeing to end its export ban on rare-earth metals and the U.S. considering allowing Nvidia to resume some chip sales[3][3]. Such steps, if finalized, would ease a few points of friction in the tech war.

Japan, in contrast, had a steadier week. After the Bank of Japan’s late-July tweak to yield curve control (allowing Japanese 10-year bond yields up to 1.0%), Japanese markets have adjusted without turmoil. The 10-year JGB yield rose to ~0.60% but remained well below the new cap, as the BOJ continued bond purchases to smooth the climb. Economic indicators out of Tokyo showed a mixed but not alarming picture. Tokyo’s core consumer inflation was 2.5% in July, slightly down from June’s 2.7%, suggesting nationwide CPI is stabilizing a bit above the BOJ’s 2% goal. Unemployment ticked down to 2.3%, a multi-year low, indicating the labor market is still very tight. Paradoxically, that low joblessness comes as other data (factory output, retail sales) point to mild weakness. It appears companies are hoarding labor despite slower demand – a positive for workers, but it means productivity is lagging. The BOJ held a policy meeting this week and, as expected, kept its rate at –0.1% and signaled it will patiently monitor inflation before any further moves. Most analysts don’t expect the BOJ to actually hike rates until perhaps end of 2025, given the delicate balance it’s managing. On the equity side, Japan’s Nikkei 225 hit a fresh 33-year high mid-week around 33,300, before settling slightly lower. Solid earnings from industrial giants and a weaker yen (still near ¥146 to the dollar) have underpinned Japanese stocks. Foreign investors have been net buyers of Tokyo shares for 14 consecutive weeks, reflecting newfound optimism in Japan’s market reforms and stable macro outlook.

Elsewhere in Asia, most markets followed the global uptick. South Korea’s KOSPI gained about +1%, led by chip and auto stocks, as cooling U.S. inflation bolstered the case for rate cuts that could boost exporters. India’s Sensex was flat, pausing after recent record highs; investors awaited data on India’s inflation and a possible U.S. decision to delay tariffs on Indian goods. Australia’s ASX 200 rose +0.6%, helped by mining companies (strong Chinese import data lifted iron ore prices) and by the general risk-on mood. In Southeast Asia, indices in Singapore and Indonesia rose modestly (~+0.5%). Currency movements were muted – the Chinese yuan held around 7.10 per dollar (with state banks reportedly supporting it), and the Japanese yen after briefly strengthening on the BOJ news, softened back to ~147 per USD by week’s end as U.S. rate cut hopes weakened the dollar slightly.

In summary, global markets navigated a minefield of news to finish the week on a high note. Investors largely chose to see the silver linings: in the U.S., a credit downgrade and soft employment are “good news” if they usher in Fed easing; in Europe, a policy mishap was swiftly corrected and inflation is coming under control; in Asia, China’s headwinds are fueling expectations of big stimulus. The result was a broad rally in equities, a drop in bond yields, and a continued retreat in commodity prices like oil. It’s a delicate equilibrium – predicated on central banks and governments responding just right to the economic signals. As August progresses, all eyes will remain on policymakers: Will the Fed indeed cut rates? Will the ECB hold fire? Will Beijing deliver the stimulus its markets are banking on? The answers will determine if this late-summer optimism endures or gives way to renewed volatility. For now, though, the markets have seized on the week’s developments as evidence that a “soft landing” – lower inflation without a deep recession – remains in play globally. The coming weeks will test that hopeful thesis against reality.

References

- [1] Monetary Policy Report – August 2025 – Bank of England

- [2] Bank of England cuts interest rates by a quarter point to 4% – CNBC

- [3] China July trade data: exports growth beats estimates as imports recover

- [4] China’s CPI inflation arrives at 0% YoY in July vs. -0.1% expected

- [5] A-Share Margin Financing Balance Tops 2 Trillion Yuan for First Time …