US Credit Downgrade, Tech Surge & China Stimulus Hopes

The Vortex – Global Market Weekly – 27 June–2 August, 2025

A shock U.S. credit rating downgrade and a dismal jobs report roiled markets—despite stellar earnings from tech giants. Europe narrowly avoided recession with meager growth and cooling inflation, while China’s leaders vowed stimulus amid deflation risks. Global stocks seesawed on hopes of central bank easing, trade developments, and an oil price slide in this eventful week.

United States – Fed Signals Easing Amid Credit Jitters

U.S. markets were whipsawed by a mix of discouraging economic signals and optimism for policy relief. Early in the week, tech earnings from giants like Apple and Amazon blew past expectations, propelling the Nasdaq to new highs. Apple reported record June-quarter revenue of $94 billion (+10% YoY)[1] and announced a massive $100 billion U.S. investment plan, news that helped its stock surge over 4%. Amazon likewise beat forecasts with $167.7 billion in Q2 revenue (up 11%), though a cautious outlook tempered its gains. The S\&P 500 briefly hit a record mid-week, boosted by these tech results and hopes that the Federal Reserve might ease policy soon.

Those hopes were fueled by hints out of the Fed. At its July 30 meeting, the Fed held interest rates steady (keeping the fed funds rate at 4.25–4.50% for an eighth straight month) but signaled it’s watching for “further evidence” of cooling inflation and hiring[2]. Crucially, Fed officials started acknowledging more downside risks. Atlanta Fed President Raphael Bostic noted on CNBC that the slowdown in hiring “adds weight to signs of a cooling trend”[2]. Behind closed doors, consensus was building that if the economy weakens further, a rate cut would be on the table soon. Markets were already inclined to believe this: even before Friday’s data, futures had about a 50–60% chance of a September cut priced in.

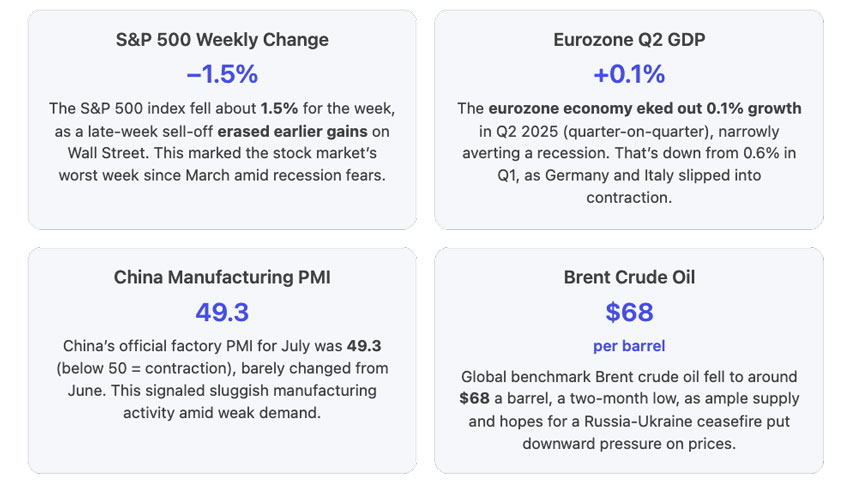

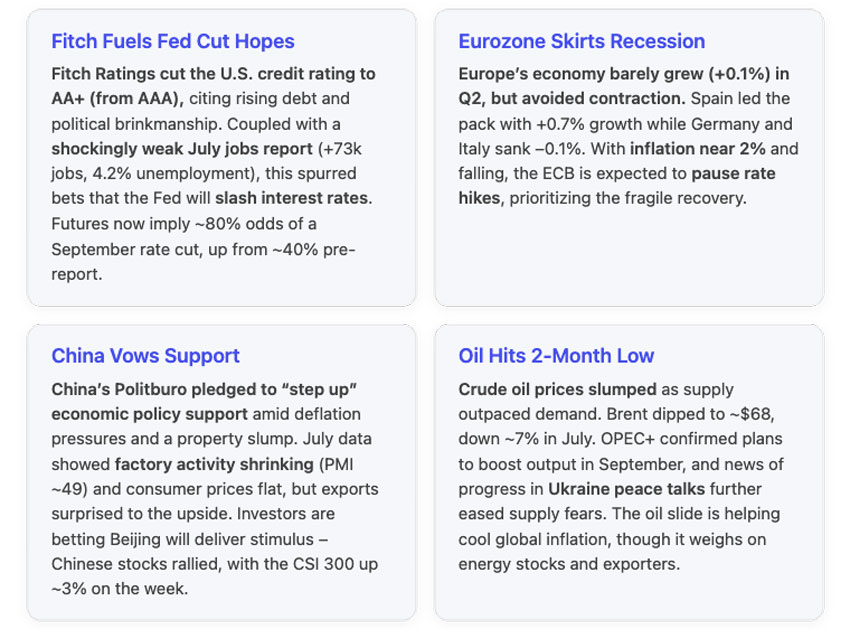

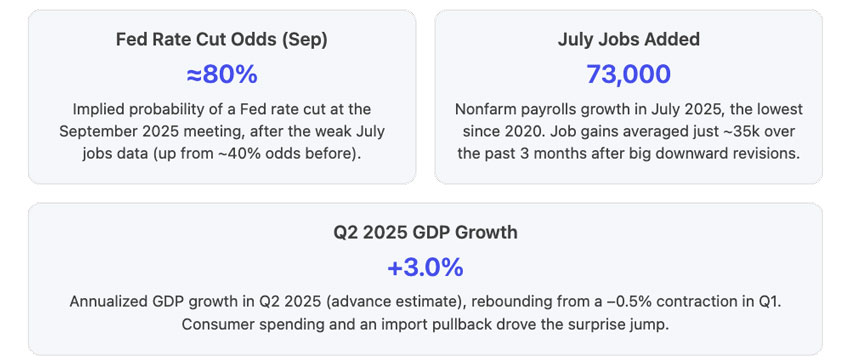

Then came a double whammy on Friday (Aug 1) that rattled confidence. First, the Labor Department’s report showed the U.S. economy added just 73,000 jobs in July[2], far below estimates (100k) and confirming a sharp downshift in hiring. What’s worse, May and June job gains were revised down by a staggering 258,000 combined. That means over the past three months, job growth averaged only ~35k – essentially stall speed for the labor market. The unemployment rate ticked up to 4.2% (from 4.1%), and the household survey even showed employment falling by 260k[2]. In short, the once-hot U.S. job market appears to be rapidly cooling off. “This is a game-changer jobs report. The labor market is deteriorating quickly,” one economist said bluntly[2]. Stocks immediately sold off on the bad jobs news, with the Dow plunging over 300 points by midday and the S\&P 500 down nearly 1%[3]. Ironically, some investors saw a silver lining: the weak report virtually guarantees Fed rate cuts. Indeed, wagers on a September cut jumped to ~80% odds after the data[2], and Treasury yields sank to multi-month lows as traders anticipated easier monetary policy.

Just as markets were digesting the employment shock, Fitch Ratings dropped a bombshell after the closing bell: it downgraded U.S. sovereign debt from AAA to AA+, citing “a steady deterioration in governance” around fiscal policy and the rising debt burden[4]. Fitch highlighted the repeated debt-ceiling standoffs and the lack of a credible long-term plan to rein in deficits. The U.S. had held a spotless AAA from Fitch for decades (S\&P’s 2011 downgrade aside), so this move was a symbolic blow. It amplified worries about U.S. fiscal sustainability at a time when the Treasury is issuing mountains of debt. While many analysts downplayed practical effects – U.S. Treasurys are still the world’s safe haven – the downgrade added to a sense of uncertainty. It was the first U.S. credit downgrade in 12 years, and it couldn’t have come at a more delicate moment. Futures initially fell on the news, pointing to a rough start for the following week. The White House blasted the downgrade as “bizarre and inept” given the economy’s resilience[4], but others noted it’s a warning shot about the U.S.’s $33 trillion debt trajectory.

In addition to these developments, the U.S. was grappling with the ongoing tariff saga. President Donald Trump had imposed sweeping “reciprocal tariffs” on over 180 countries earlier in the year (with rates up to 50%), then paused the hikes for 90 days. That pause expired August 1. At the last minute, Trump signed an executive order that adjusted many tariff rates and set a new structure: most non-allied countries face a 15% baseline tariff, while certain nations get even higher duties (e.g. 40% on any goods deemed “transshipped” to dodge rules)[5][5]. Notably, the EU, Japan, and others who struck trade frameworks with Washington will be subject to the “modified” rates (~15–20%)[5], avoiding the worst-case scenario. Trump declared “the August First deadline…stands strong,” emphasizing his hard line[5]. Markets have grown somewhat desensitized to tariff headlines, but this formal tariff reboot is another headwind for businesses and a wildcard for inflation. On Friday, new tariffs on Canada also kicked in (raising duties on Canadian exports to 35%[5], exempting USMCA-covered items), showing Trump’s willingness to spar even with allies.

Amid all this, U.S. economic data wasn’t entirely grim. The Commerce Department’s initial Q2 GDP estimate showed the economy grew at a 3.0% annual pace[2], a robust rebound from the Q1 contraction (–0.5%). However, the details were mixed: much of the growth came from a drop in imports (after companies stockpiled before tariffs in Q1) and a buildup in inventories, rather than surging domestic demand. Underlying consumer spending was positive but modest, and business investment actually fell in some areas. Economists like Gregory Daco warned that the strong Q2 headline was “largely a mirage” and that growth would likely fizzle to <1% in Q3. In other words, by late July the writing was on the wall that the economy’s momentum is slowing – a message only reinforced by the awful July jobs report. This explains why Fed officials have pivoted from talking about inflation risk to also acknowledging growth risks. Fed Chair Jerome Powell, speaking on July 30, noted that if the job market weakens more than expected or inflation ebbs faster, “we have policy space to respond appropriately.” In plain English: the Fed is opening the door to rate cuts.

Investors are now fully pricing in a Fed rate cut on Sept. 17, which would be the first reduction since late 2024. The 10-year Treasury yield ended the week around 4.27%, down from ~4.5% just two weeks ago, reflecting those expectations. The dollar index also slid to a one-month low. In the stock market, the late-week sell-off left the S\&P 500 down about 1.5% for the week[3] – its first weekly loss since May – even after hitting a record on Wednesday. Still, the index closed out July with an impressive +4.9% gain for the month, and is up ~20% YTD, thanks largely to Big Tech’s strength. The Dow dropped around 1% for the week. The Nasdaq Composite shed 2% on the week as high-valuation tech names were whipsawed by rate expectations and some profit-taking. Volatility spiked: the VIX jumped to 19, its highest in three months. All said, the mood on Wall Street has shifted to “cautiously optimistic.” Investors are encouraged that the Fed will ride to the rescue with rate cuts, but the sudden cracks in the economy (jobs) and surprises from policymakers (Fitch, tariffs) have injected fresh volatility. The next few weeks – with more inflation data and Fed speeches – will be crucial to see if the Fed indeed validates the market’s bet on easier policy.

European Union – Economy Stalls but Relief on Trade and Inflation

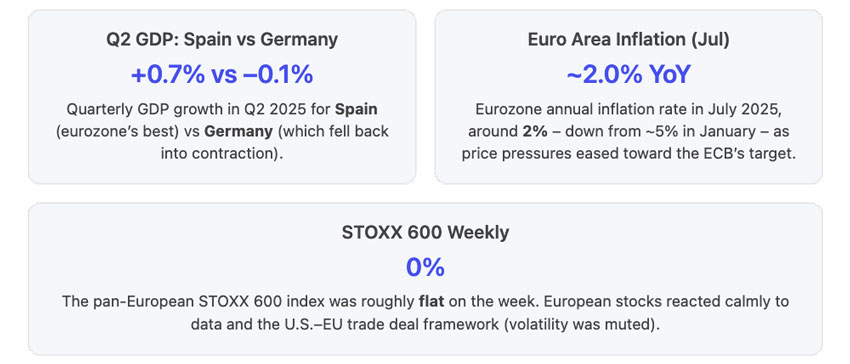

Europe’s economy ground to a near-halt in Q2, though it fared slightly better than feared. According to Eurostat’s flash estimate, eurozone GDP grew just +0.1% quarter-on-quarter[6] in Q2 2025 (0.2% for the EU as a whole). That’s a sharp slowdown from Q1’s 0.6% pace and barely above stall speed – but it did mean the euro area dodged a technical recession (defined as two negative quarters). The performance was very uneven across member states. Spain outperformed with a strong +0.7% jump in Q2 GDP[7], bolstered by robust consumer spending and a rebound in tourism and investment. France also surprised to the upside with +0.3%, its best in nearly a year[7][7], as domestic demand held up. In stark contrast, Germany’s economy contracted –0.1%[7] (confirming a return to recession for Europe’s largest economy, which also shrank slightly in Q1) and Italy’s GDP fell –0.1%[7], undercut by weak industrial output. This divergence – Southern Europe growing while the traditional engines in the North sputter – continued a trend seen earlier in the year.

On the inflation front, Europe got some relief. Eurozone headline CPI for July is estimated around 2.0% year-on-year, a dramatic comedown from rates above 5% at the start of the year. In fact, France’s inflation has slowed to about 0.8% – one of the lowest in the bloc – thanks to energy price declines and government subsidies. Even in Germany, inflation is moderate (~2–3%). Core inflation (ex. food & energy) remains stickier at ~2.3%, but has at least stopped rising. This broad easing of price pressures, combined with the frail growth, is reinforcing expectations that the European Central Bank will extend its pause on rate cuts (the ECB deposit rate is 2.0% and was left unchanged in July after eight consecutive cuts). ECB President Christine Lagarde said last month the bank is “in a good place” on policy, and recent data vindicate that patient stance. Markets aren’t pricing in any further rate moves at the next ECB meeting (Sept 10) – neither cuts nor hikes – as officials gauge whether inflation will settle near target without more intervention.

Besides macro data, a major overhang for Europe – trade tensions with the U.S. – saw a tentative resolution. Over the July 27 weekend, the EU reached a trade framework agreement with the U.S. that helped avert the worst of Trump’s looming tariff threats[6]. Under the understanding, the U.S. will impose a general 15% tariff on EU goods (instead of the 25–30% initially signaled), and punitive 250% tariffs on European pharmaceuticals were dropped[6]. In return, the EU committed to invest hundreds of billions in U.S. energy projects and made concessions on certain imports. This deal came just in time – hefty U.S. auto tariffs were set to hit, which could have hurt German carmakers. European officials breathed a sigh of relief at the compromise. As one analyst put it, it’s “more favorable than expected” for Europe[6], even if the U.S. had the upper hand. European markets reacted calmly; the euro even ticked up slightly after the announcement, and European equities stabilized. The STOXX 600 saw little movement on the news[7], indicating that much of the trade conflict was already priced in and that investors were relieved to avoid escalation. There is still some wariness – a 15% tariff is not trivial, and sectors like European autos and luxury goods will face headwinds – but it’s a far cry from a full-blown trade war.

Another positive development for Europe: energy prices have remained benign. Natural gas storage is high and prices are a fraction of last year’s levels, reducing costs for industry and consumers. And as noted, oil fell further this week, which should help lower transportation and heating costs across Europe. This is a stark difference from 2022’s energy crunch and is boosting consumer real incomes now. Also notable, the European labor market remains resilient. Unemployment in the eurozone stayed at a record-low 6.2% in June–July. In many countries, worker shortages persist, which is supporting wages. For example, Germany’s jobless rate is ~5.7%, up slightly but still low historically, and in Spain unemployment is at its lowest since 2008, thanks to the tourist boom. Strong employment, coupled with easing inflation, means consumers are a bit more confident than earlier in the year.

Financial markets in Europe ended the week steady overall. The German DAX index slipped about 0.3% across the week, weighed down by some weak earnings in the chemicals sector and the poor German GDP data. The French CAC 40 rose roughly 0.5%, helped by upbeat results from luxury giant LVMH (which jumped 3% after an analyst upgrade). Italy’s FTSE MIB recovered from a mid-week bank stock rout – triggered by an unexpected windfall tax announced then rescinded by Rome – to finish about flat. The pan-European STOXX 600 was literally unchanged (0.0%)[7]. Investors seemed to adopt a “wait and see” attitude, balancing the weak growth outlook against the positive trade news and prospect of global rate cuts. European bond yields were little changed: the German 10-year Bund yield hovered around 2.60%, and Italian 10-year yields around 4.15%, essentially stable for the week. The euro currency drifted slightly higher to ~$1.17, benefiting from the U.S. dollar’s post-Fed dip.

In summary, Europe is in a holding pattern: growth is almost flat, but a feared recession has so far been dodged. Inflation is coming under control, easing pressure on the ECB to act further. And external drags – like trade fights and energy shocks – have lessened for now. That’s not to say Europe is out of the woods; Germany’s struggles are a big concern, and any faltering in U.S. or Chinese demand could still tip Europe over. But relative to the dire scenarios of last year, the picture is one of cautious stability. The focus now turns to whether Europe can reignite some growth (perhaps via fiscal stimulus in Germany or EU-wide investments) and how it navigates the still uncertain global environment. Markets, at least, seem comfortable with Europe’s slow-growth, low-inflation equilibrium for the moment.

Asia – China Seeks Stimulus, Japan Tweaks Policy as Markets Ride High

Asian economies sent mixed signals this week, with China’s slowdown prompting calls for stimulus while Japan made a subtle shift in its ultra-easy monetary stance. Equity markets across Asia, meanwhile, largely took cues from global trends, rallying early in the week and then cooling a bit by Friday.

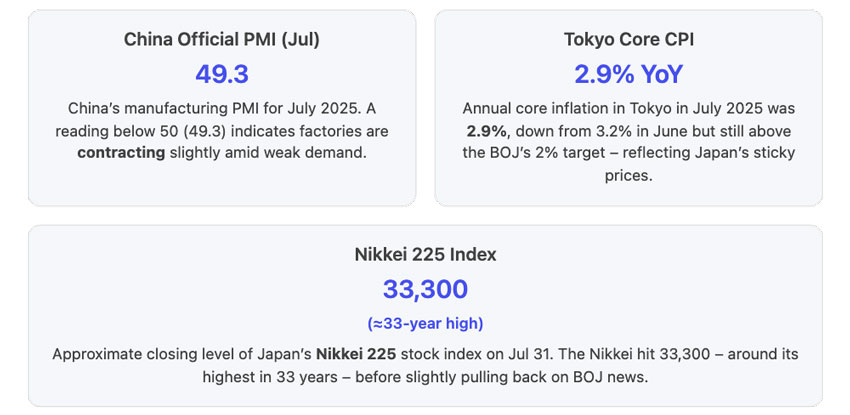

In China, the data drip continues to point to an economy struggling to regain momentum. The latest indicators for July showed both manufacturing and consumer sectors under pressure. The official Manufacturing PMI came in at 49.3, stuck in contraction territory for a fourth month. Output and new orders remained weak as domestic demand faltered and global orders softened. Likewise, estimates suggest overall GDP growth in Q3 is off to a tepid start – this after Q2’s 5.2% YoY growth, which was propped up by net exports. The property market remains a significant drag; home sales and prices are still falling in many cities, and property investment is down double-digits percent from a year ago. There’s a real risk that China could slide into deflation: consumer prices in July were roughly flat (0% YoY) and producer prices have been falling ~5% YoY. It’s no wonder then that China’s leadership is pivoting to stimulus mode.

On July 30, Beijing’s powerful Politburo held its mid-year economic meeting and struck a much more supportive tone. The leaders vowed to “step up” policy support and explicitly acknowledged “risks of deflation” and weak demand[8]. This was a notable change from their April meeting, where they sounded more relaxed. The Politburo promised measures to boost consumption, support the housing market (“meet reasonable housing demand”), and tackle youth unemployment (which hit a record ~21% recently). They also talked about managing “disorderly competition” and preventing price wars – code for propping up prices and profits in sectors suffering from overcapacity, like steel. Importantly, the Politburo did not announce a massive stimulus package on the spot; instead, they signaled readiness to use tools if needed (keeping policy “steady with flexibility”). Analysts read this as meaning the People’s Bank of China (PBoC) could cut interest rates or banks’ reserve ratios in coming months, and fiscal authorities may accelerate infrastructure spending or issue more special bonds. One concrete step: regulators eased some home-buying restrictions in big cities this week, aiming to spur property sales. The government also instructed banks to extend loan relief to property developers to avoid a collapse like Evergrande’s.

Investors in China are already front-running the anticipated stimulus: Chinese stocks have been on a tear. The Shanghai Composite Index climbed for an eighth straight session, and the CSI 300 (blue-chip index) is up about 3% this week and over 10% for the month. That rally added roughly $300 billion in market cap this week alone. Trading volumes in Shanghai hit multi-year highs as retail investors pile in, emboldened by state media’s positive spin. This surge has indeed caught Beijing’s attention – officials have started warning about speculative excess (memories of the 2015 boom-bust are fresh). Notably, the stock frenzy is being fueled by expectations that Beijing will unleash more stimulus and by flush liquidity in the system (household savings looking for yield). There’s also some relief that U.S.–China trade tensions haven’t worsened: on July 29, Washington and Beijing agreed to extend their tariff ceasefire beyond August[8], delaying a potential re-escalation. In fact, China’s exports in July unexpectedly jumped ~7.2% YoY, which analysts attribute to exporters rushing shipments ahead of any future tariff changes[8]. That export bump is likely temporary, but it gave the economy a slight boost. All told, China’s near-term outlook hinges on policy action: will the government deliver meaningful stimulus to shore up growth? The Politburo hints and market optimism suggest they will, but the scale remains to be seen. Until then, the risk is that the economic malaise continues – and perhaps deepens – if confidence doesn’t improve.

Turning to Japan, the story is almost the mirror image: the economy has been growing modestly, and inflation is actually above target, prompting the central bank to carefully inch toward policy normalization. This week Japan delivered a surprise of its own. On July 28, the Bank of Japan adjusted its yield curve control (YCC) policy, effectively allowing long-term interest rates to rise a bit more. Specifically, the BOJ kept its target for the 10-year government bond at ~0%, but changed the hard cap from 0.5% to a more flexible 1.0%. In practice, the BOJ said it would tolerate the 10-year yield moving up to 1% before intervening heavily. This move was unexpected in timing (coming in between scheduled meetings) and was seen as a response to growing inflationary pressures. Tokyo’s core CPI was 2.9% in July and 2.5% in August – that’s above the 2% goal for well over a year now. With the job market tight (unemployment in Japan fell to 2.3% in July, the lowest since 2019) and wages finally rising around 2–3%, the BOJ is carefully preparing for an eventual interest rate hike. Governor Kazuo Ueda still emphasizes a cautious approach – he doesn’t want to choke off Japan’s fragile recovery or cause a spike in the yen – but the YCC tweak shows the BOJ is inching away from its ultra-loose stance.

The immediate market reaction in Japan was volatile but contained. The yield on 10-year JGBs jumped from ~0.45% to about 0.60% after the announcement, its highest in years. The yen briefly strengthened to ~145 per dollar in knee-jerk fashion (since higher yields make the currency more attractive), but then weakened back to ~147 as global dollar dynamics took over. The Nikkei 225 stock index, which had been on a stellar run to 33-year highs (hitting ~33,300 this week), pulled back slightly on Friday, ending around 32,700 – still up about 1% for the week. Japanese bank stocks popped 2–3% on the BOJ’s hint at higher rates (since that can improve bank profits), while exporters like Toyota dipped on the yen’s swings. Big picture: Japan’s economy is doing reasonably well. Q2 GDP growth likely came in around +0.3% QoQ (annualized ~1.2%), and consumer demand has held up despite higher prices. The BOJ is trying to thread the needle by adjusting policy incrementally, hoping to avoid any shocks. Most analysts expect the first actual BOJ rate hike (lifting its –0.1% policy rate) might come in October or December if current trends persist. In the meantime, Japan benefits from stable global conditions and strong regional trade.

Elsewhere in Asia, other markets were mixed but generally stable. South Korea’s KOSPI index rose ~0.5% on the week, aided by chipmakers after Samsung gave an optimistic guidance. India’s Sensex hit a fresh all-time high mid-week, above 68,000, before profit-taking left it flat by Friday. India’s economy is one of the few accelerating, with strong services PMI readings. Southeast Asian markets (Indonesia, Malaysia, Thailand) saw modest gains of 0.5–1%, tracking the global tech-led rally early in the week. Notably, emerging Asian currencies got a lift mid-week when the dollar fell post-Fed: the Korean won and Thai baht each gained ~1%. However, by week’s end the moves faded. Oil-importing nations in Asia welcomed the continued drop in crude prices – a boon for trade balances and inflation. For example, Thailand’s inflation is now under 1%, allowing its central bank to hold rates. Central bank actions were few this week, but the Philippines did cut its policy rate by 25 bps to 5.00%, citing easing inflation (now ~2%) and the need to support growth.

In summary, Asia finds itself at a crossroads. China is stimulating and trying to rekindle growth after a disappointing first half. Japan is cautiously pulling back its long-running stimulus as inflation finally perks up. Other Asian economies are either locking in stability (South Korea, Taiwan) or enjoying post-pandemic rebounds (India, Southeast Asia) with an eye on global headwinds. The region’s equity markets are doing well – the MSCI Asia ex-Japan index is up ~9% year-to-date – underpinned by the global risk-on sentiment and prospects of U.S. rate cuts. Yet, risks remain: China’s slowdown could spill over to trade partners, and any U.S. recession would hit Asian exporters hard. For now, though, the tone is optimistic. Investors are riding the wave of ample liquidity and policy hopes, making Asia one of the better-performing regions in 2025 so far. The coming weeks will be crucial to see if China’s promised support measures materialize and whether Japan’s policy tweak is followed by any market turbulence or if it’s absorbed smoothly. Asia’s economic balancing act continues, but this week showed that policymakers in the region are proactive and markets are mostly taking changes in stride.

References

- [1] Apple reports third quarter results – Apple

- [2] Jobs report July 2025: U.S. added just 73,000 jobs, prior months … – CNBC

- [3] Dow Tumbles as Weak July Jobs Report and Fresh Tariffs Spark Fears of U …

- [4] Fitch Downgrades US Credit Rating Amid Fiscal Face-Offs. Here’s Why It …

- [5] Trump modifies tariffs ahead of deadline, targets transshipment with 40 …

- [6] German, Euro zone GDP Q2 2025 – CNBC

- [7] Eurozone GDP growth slows to 0.1 percent in Q2 2025 as Spain leads …

- [8] China’s Leaders Vow Support for Economy, Crackdown on Disorderly …