Fed Hints, Trade Deal & China’s Surge

The Vortex – Global Market Weekly – 17–23 July, 2025

Central bankers turned dovish, tech stocks rode a roller coaster, and Chinese markets soared in this eventful week. From Fed Chair Powell hinting at rate cuts and sending the Dow to a record high, to Europe clinching a major trade deal and China’s stocks hitting decade highs despite economic headwinds, the week of August 17–23, 2025, saw pivotal shifts across the U.S., EU, and Asia.

United States – Fed Shift Sparks Market Rally

The U.S. financial narrative this week was dominated by the Federal Reserve’s changing tone and a euphoric stock market response. In a much-anticipated address on Friday (Aug 22) at the Jackson Hole symposium, Fed Chair Jerome Powell strongly hinted that the Fed is ready to ease monetary policy. Powell noted that rising downside risks to employment and cooling inflation “may warrant adjusting [the Fed’s] policy stance,” acknowledging that interest rates are already at restrictive levels[1]. Investors took this as confirmation that the Fed will likely cut interest rates in September, which would be the first rate reduction of 2025.

Markets reacted with relief and enthusiasm. Stocks surged on Friday, capping a roller coaster week. The Dow Jones Industrial Average jumped ~850 points (+1.9%) in one day, reaching a record closing high of 45,632 (its first record of the year)[2]. The S\&P 500 leapt 1.5% on Friday, just a hair below its own record, and the Nasdaq Composite rebounded 1.9%[1]. This powerful rally erased earlier losses and meant the Dow and S\&P notched their third consecutive weekly gain (up +1.5% and +0.3% for the week, respectively)[1]. Investors, who had been nervous all week awaiting Powell’s remarks, breathed a sigh of relief. Rate-sensitive sectors led the charge: giant tech stocks, which had slumped mid-week, roared back by Friday. Tesla stock soared 6%, while Alphabet and Amazon climbed ~3%. Homebuilder and real estate stocks also popped 5–8% on expectations that mortgage rates will fall with Fed easing.

Earlier in the week, the mood was more cautious. Hawkish signals from the Fed’s July meeting minutes (released Wednesday) had given investors pause, as officials still saw upside inflation risks outweighing growth risks[3]. Some economic data was mixed: for example, weekly jobless claims came in slightly higher than expected (229,000 new claims), hinting at a mild cooling in the labor market, even as business surveys showed resilience. But all that was overshadowed by Powell’s dovish pivot. Notably, futures markets quickly priced in an ~83% probability of a September rate cut after his speech[4] (up from ~60% a week prior). The U.S. 10-year Treasury yield fell sharply, ending around 4.26% (down from 4.33%)[1]. The dollar also weakened on the prospect of lower rates, hitting a one-month low and boosting gold prices (gold futures rose ~1.1% to $3,415/oz).

Outside of the Fed, technology sector news provided its own drama. Mid-week, tech shares stumbled amid talk of an “AI bubble” losing air. A report from MIT and comments by OpenAI’s CEO Sam Altman cautioned that many companies see “zero return” from generative AI so far[3], which sparked a sell-off in high-flying AI stocks on Tuesday: Nvidia fell over 3%, and other AI-exposed names sank 5–9%. The Nasdaq was down as much as 1.2% through Thursday[3]. However, strong earnings from some tech firms (e.g. chipmaker Analog Devices beat forecasts) and the Fed-induced rate optimism helped the sector quickly recover. By week’s end, the Nasdaq’s loss was pared to –0.6%. In other corporate news, an unusual development saw President Donald Trump announce plans for the U.S. government to take a 10% stake in Intel (to bolster domestic chip production); Intel shares jumped 5.5% on the news[1]. Meanwhile, cryptocurrency markets mirrored the resurgence in risk appetite: Bitcoin rebounded to ~$117,000, up from $112K earlier in the week, as investors rotated back into speculative assets post-Fed speech.

Energy prices in the U.S. eased, helping the inflation outlook. U.S. oil benchmark WTI briefly dipped to its lowest levels since early June (near $63/barrel). Brent crude, the global benchmark, hovered around $66–68 on Aug 23 – marking about a 7% drop over the past month. This slide in oil, driven by ample supply and weakening demand, is a potential boon for American consumers, likely translating to cheaper gasoline. For the Fed, softer oil prices provide breathing room on inflation, reinforcing the case for a rate cut.

European Union – Stocks Rise on Trade Deal & Data Surprises

European markets had a generally upbeat week, powered by a major breakthrough in trade and some encouraging economic signals. The pan-European STOXX 600 index rose ~0.7% over the week, and Britain’s FTSE 100 index not only touched fresh record highs but also logged its best weekly performance since May[4]. Several factors drove the optimism:

- EU-U.S. Trade Deal: Officials in Brussels and Washington unveiled details of a sweeping trade agreement reached in principle last month. The EU agreed to invest $750 billion in U.S. energy projects and at least $600B in U.S. industries[1]. In return, the U.S. scaled back tariff threats: across-the-board tariffs on European goods will be capped at 15% (instead of a threatened 30%), and a proposed 250% tariff on European pharmaceuticals was scrapped[1][1]. This resolution of trade tensions lifted European market sentiment, especially in affected sectors. Pharmaceutical stocks in Europe bounced — the STOXX Europe Pharma index rose ~0.6% as tariff fears eased[1]. Auto stocks also saw relief, though gains were muted because the auto tariff cut to 15% will be conditional on EU policy changes[1]. Still, the trade peace removed a major cloud of uncertainty, prompting Deutsche Bank analysts to call it a “more dovish outcome than expected” for Europe’s outlook.

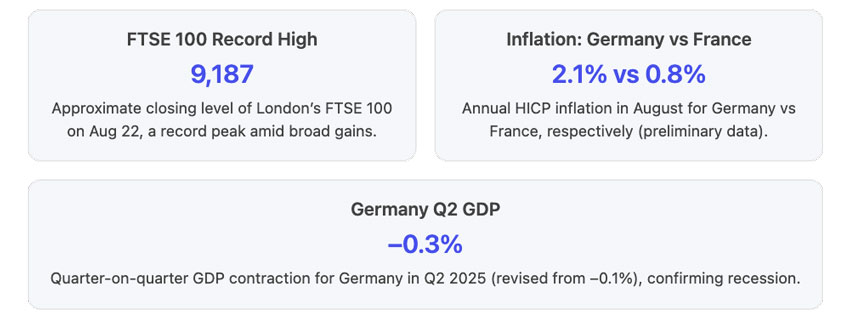

- Economic Data and ECB: Europe’s economic news was mixed but with bright spots. In the UK, a flash Purchasing Managers’ Index (PMI) showed the strongest business activity in a year, boosting confidence. Retail and consumer stocks in London rallied on that data. Combined with gains in mining and banking shares, this helped London’s FTSE 100 set record highs four days in a row. Eurozone PMIs for August also ticked up modestly, signaling that manufacturing and services decline may be bottoming out. However, not all data were positive: a revised reading confirmed Germany’s Q2 GDP shrank –0.3% (quarter-on-quarter)[5], worse than initially thought and marking a second straight quarter of contraction (a technical recession). Inflation readings were similarly divergent: Germany’s harmonized inflation picked up to 2.1% in August (from 1.8% in July)[2], while France’s inflation slowed to just 0.8%[6]. These trends, alongside European Central Bank (ECB) minutes revealing a split outlook, bolstered the case that the ECB will likely hold interest rates steady at its next meeting[1][1]. In the UK, headline CPI was 3.8% in July (slightly up from June) with stubborn core price pressures[4], complicating the Bank of England’s path. Overall, the data suggest a Europe that is avoiding the worst-case recession scenario but still growing slowly, giving central bankers room for patience.

European equities benefitted from global rate-cut optimism as well. The prospect of Fed easing fueled hopes that central banks worldwide might pivot to more accommodative stances, helping Europe’s interest-sensitive sectors. Bank stocks were flat (future lower rates can crimp bank margins), but other sectors outperformed. Travel & leisure companies gained as lower borrowing costs could boost consumer discretionary spending. Commodity-linked stocks also rallied: with China’s stimulus hopes (important for European luxury and industrial goods demand) and the trade deal lifting sentiment, French luxury giants and German industrials had a solid week.

By Friday, European indices closed higher across the board. The German DAX and French CAC 40 each gained ~1% for the week, and the UK’s FTSE 100 set a new record high around 9,187 points[7]. The euro and British pound both strengthened ~1% against the U.S. dollar after Powell’s speech (EUR/USD near 1.17), reflecting expectations of a smaller U.S.–Europe interest rate gap. A stronger euro/pound can be a headwind for European exports, but in this case it was seen as a sign of confidence in Europe’s stability. In summary, Europe ended the week on a positive note: trade uncertainty eased, recession fears tempered by slightly better data, and central banks likely to stay supportive barring any new inflation surprises.

Asia – China’s Stock Boom vs Economic Gloom

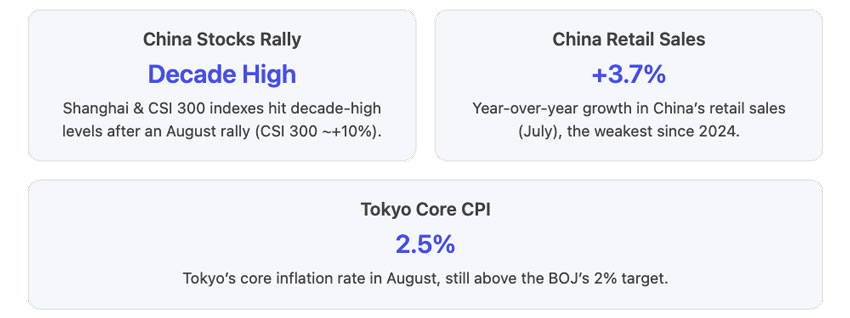

Asian financial news was headlined by a paradox in China: surging stock prices in the face of weakening economic data. China’s economy flashed more warning signs that its post-pandemic recovery is faltering. Key July indicators were underwhelming: retail sales rose just +3.7% year-on-year, the slowest pace since late 2024[8], and industrial output growth slowed to +5.7% (an eight-month low)[8]. Perhaps most worrying, fixed-asset investment in Jan–Jul grew only +1.6%[8], dragged by a 12% plunge in property sector investment[8] amid China’s ongoing real estate slump. In fact, new home sales by floor area dropped ~4% from a year earlier, and consumer inflation was roughly 0.0% (flat year-over-year in July) – signaling a risk of deflation as domestic demand stays soft. This week also brought another sign of property sector distress: Country Garden, one of China’s largest developers, missed a bond interest payment, raising fears of default on its $16 billion in overseas debts. Although a state-backed guarantor said it would cover the payment to avoid default, the news underscored the deepening housing market woes.

Yet, in sharp contrast, Chinese stocks staged a remarkable rally. The CSI 300 index (mainland China’s blue-chip index) surged about +4% for the week[3] and roughly +10% over the month of August, reaching decade-high levels[7]. In Hong Kong, the Hang Seng Index rose ~1%, and Shanghai’s Composite gained similarly. Investors seem to be betting that weak data will force Beijing’s hand to unleash more economic stimulus. There is also a flood of liquidity in China’s financial system – bank deposits are high and seeking returns – which is fueling speculation in equities. Indeed, margin financing by Chinese traders has climbed to multi-year highs: outstanding margin loans hit ¥2.18 trillion, the most since 2015[7]. This credit-fueled optimism is reminiscent of past booms. For now, Beijing has signaled willingness to support growth (for instance, by easing home purchase restrictions in some cities and cutting banking rates slightly), but has not yet unleashed any massive stimulus. Still, the stock market is front-running potential policy moves. As a result, China’s markets are booming despite the economy’s aches – a divergence that some analysts warn is unsustainable without concrete improvements. Nomura’s strategists noted that the equity surge alone won’t fix China’s challenges, though it does improve sentiment in the short term.

Elsewhere in Asia, Japan’s economy and markets showed more traditional dynamics: signs of cooling inflation and a tight labor market, with stocks reflecting caution. Japan reported that core inflation in Tokyo (a leading indicator for nationwide CPI) was +2.5% in August[5] – a third monthly decline but still above the Bank of Japan’s 2% target. This marks well over two years that inflation has exceeded 2%, keeping pressure on the BOJ to consider tightening policy. However, the BOJ remains very cautious, especially with mixed economic signals. Notably, Japan’s unemployment rate fell to 2.3% in July, the lowest since 2019[5], indicating an even tighter job market than expected. Yet retail sales rose just 0.3% y/y[5] – essentially flat – suggesting that rising living costs are making consumers cautious. Industrial output also fell 1.6% in July[5], partly due to U.S. tariffs denting car production. These cross-currents (low joblessness but weak spending) highlight the dilemma for the BOJ. About two-thirds of economists now expect the BOJ to raise interest rates by year-end[5], but Governor Ueda has emphasized the need to see durable inflation driven by wages. Most likely, the BOJ will stay on hold for a bit longer, waiting for clearer evidence before any move. Japanese stocks reflected this uncertainty: the Nikkei 225 slipped ~1.7% for the week[3] after a strong summer, as investors took profits and reacted to the prospect of slightly higher rates ahead.

Other Asian markets were mixed but generally benefited from the global trends. In India, stocks were flat as domestic optimism met global trade worries. Australia’s ASX 200 hit record highs during the week, boosted by strong corporate earnings and the tech rally spillover[3]. Emerging markets in Southeast Asia also saw modest gains, helped by the Fed’s dovish turn which eases pressure on their currencies. One notable central bank move: The Philippines’ central bank cut interest rates by 0.25% to 5.00%, citing easing inflation and the need to support growth[5][5] – aligning with the broader 2025 trend toward monetary easing.

Summary: The week of August 17–23, 2025 brought significant developments in global economics and markets. The U.S. Federal Reserve’s dovish signal was the catalyst for a worldwide rally, propelling stocks to new highs and pushing bond yields lower. In Europe, a combination of an EU-U.S. trade deal and slightly better economic data lifted sentiment, despite ongoing recession fears in Germany. Asia presented a tale of two narratives – China’s stock market soared on stimulus hopes even as its economic slowdown deepened, while Japan grappled with mixed signals of strong employment but weak spending. Major themes in tech, banking, and energy intertwined across regions: tech stocks gyrated with the evolving AI narrative, banks eyed the interest rate outlook warily, and oil prices at two-month lows provided relief on inflation even as they pointed to cooler demand. It was a week where policy expectations often overshadowed current economic realities, and investors largely bet on support from central banks and governments to keep the momentum going. As summer turned to autumn, all eyes are on whether this policy-driven optimism will be validated in the coming weeks – or if markets have gotten a bit ahead of the economic fundamentals.

References

- [1] Record Margin Debt in Chinese Stocks Signals Risk-On Momentum for …

- [2] Stock Market News, Aug. 22, 2025: Dow Gains as Fed Chair Powell Opens …

- [3] Jerome Powell and the Fed: 80%+ Chance of Interest Rate Cut in September

- [4] Market Watch: FTSE 100 posts best week since May

- [5] Japan’s Output Falls as US Tariffs Bite, Inflation Slows

- [6] French Preliminary Inflation at +0.8% in August, Slightly Below Forecast

- [7] Chinese Stocks at Decade High Lure Hesitant Retail Investors

- [8] China’s Factory Output, Retail Sales Growth Slump in Blow to Economy