Fed Cut Hopes Lift Global Markets as Trade Tensions Simmer

The Vortex – Global Market Weekly – August 31– September 6, 2025

Summary: Global economic and financial news for the week Aug 31 – Sep 6 was marked by rising expectations of the first U.S. interest rate cut of 2025, which buoyed markets to fresh highs even as trade war tensions and mixed economic data kept investors on alert. In the United States, a sharply weaker jobs report fueled bets that the Federal Reserve will ease policy at its mid-September meeting, sending stocks to record levels and bond yields to multi-month lows. Over in the European Union, leaders struck a trade deal with Washington to cap tariffs at 15%, averting a worse escalation and lending relief to markets as the region’s economy showed resilience (with improved PMI readings and inflation near target) ahead of an ECB decision. Meanwhile, across Asia, Japan’s stock market surged to 33-year highs on optimism over U.S. rate cuts and domestic growth, even as China’s economy continued to lose momentum – strengthening the case for Beijing to roll out fresh stimulus. The following is a region-by-region breakdown of the week’s biggest headlines, complete with key data, expert insights, and visual highlights.

United States: Weak Jobs Fan Rate-Cut Bets as Stocks Hit Highs, Yields Slide

Jobs Data Signals Slowdown: The U.S. labor market showed clear signs of cooling, triggering a wave of speculation that the Federal Reserve will finally ease up on its tight monetary policy. The Labor Department’s August employment report revealed that nonfarm payrolls rose by just 22,000 – a fraction of consensus estimates (~75,000) and the weakest monthly gain in over three years[1]. In addition, the unemployment rate ticked up to 4.3% (from 4.2% in July)[1], its highest since mid-2024. Hiring has essentially hit “stall speed,” as one Goldman Sachs economist put it, noting the “breadth of job gains remains poor”. Indeed, revisions showed that June employment actually fell slightly, and job openings have been steadily declining – by July there were slightly fewer vacancies than job seekers for the first time since the pandemic[2][2]. While a deteriorating labor market raises concerns about the economy’s health, investors took it as good news for interest rates. The weak payrolls “strengthens the belief” that the Fed will cut its benchmark rate at the upcoming September 17 meeting[1]. Traders in federal funds futures assigned a 99%+ probability of a quarter-point rate cut this month[3], a dramatic shift from just a few weeks ago. Fed Chair Jerome Powell had already hinted in late August that if growth cooled, a cut could be warranted[1]. Now, with what one analyst called “the job market … looking the wobbliest since the pandemic”, the case for Fed easing appears to be sealed. At the same time, inflation – though slightly above target – is seen as contained (headline CPI +2.9% y/y in August, core 3.1%), giving the Fed cover to focus on employment. Still, Fed officials have balanced this dovish pivot with caution. Powell noted that while the labor supply-demand is “in balance,” it’s a “curious” equilibrium achieved by both fewer openings and fewer workers, and thus “fragile”[2]. In short, the Fed appears poised to deliver a long-awaited rate cut, but will do so while carefully watching that the slowdown doesn’t become a downturn.

Stocks Soar, Then Steady: U.S. equity markets rallied on the building Fed cut hopes, with major indexes notching new records during the week. On Thursday (Sep 4), the S\&P 500 surged 0.8% to close at 6,502.08 – its 21st record high of 2025[3]. The Nasdaq Composite jumped 1% to 21,705.69, also a record, boosted by strength in semiconductor shares[3]. The blue-chip Dow Jones Industrial Average climbed 0.8% ( +350 points) to 45,621.29[3], finally eclipsing its previous peak. Investors poured into risk assets on optimism that lower rates will support valuations. “All three major stock indexes ended in positive territory” ahead of the jobs report, noted a Zacks analyst[3]. Even after Friday’s slight pullback – stocks initially rallied on the weak jobs number, then eased as traders consolidated gains – the S\&P 500 and Nasdaq still posted modest weekly gains[1] (their 6th weekly advance out of the past 7), while the Dow was down just a tad[1]. Notably, each index hit an intraday all-time high on Friday morning before gravity reasserted[1]. The prospect of Fed easing sent the 10-year Treasury yield tumbling to 4.06%, its lowest since April[1], which in turn bolstered rate-sensitive sectors like housing and utilities. Market volatility remained low – the VIX fell to ~15[3] – as the “Fed put” calmed fears. On the corporate front, a few major earnings and stock moves caught attention. Broadcom (AVGO), a bellwether chipmaker, reported blockbuster results that handily beat estimates, thanks to booming demand for its AI-related semiconductors[1][1]. Broadcom’s stock surged 9% on Friday[1], and its bullish forecast lifted the broader Philly chip index by 1.7%[1]. Rival Nvidia (NVDA) saw shares dip ~3%[1] this week (after a meteoric run earlier in the summer), as some investors took profits, but the AI chip theme remains a key driver of 2025’s market gains. In retail, Lululemon (LULU) plummeted 19% – the yoga apparel maker issued a weak outlook, citing sluggish U.S. sales and tariff-related cost pressures[1][1]. On the flip side, Tesla (TSLA) jumped about 4% after unveiling a new decade-long performance pay plan for CEO Elon Musk that could be worth up to $1 trillion if ambitious targets are met[1][1]. Broadly, the equity rally has been supported by better-than-feared Q2 earnings and hopes that any recession will be mild. With the S\&P 500 up roughly 11% year-to-date, some strategists warn of “stretched” valuations, but so far the lure of potential Fed rate cuts is overpowering those concerns.

Fed and Trade Policy in Focus: While Fed watchers anticipate a policy shift, the White House continued to make economic waves of its own. President Donald Trump intensified his expansive tariff campaign, ordering modifications to his “reciprocal tariffs” program that initially took effect in April. In a move announced this week, Trump added new tariffs on several countries: a 20% tariff on all Chinese imports (justified as countering the fentanyl drug trade) and steep levies on others – 25% on Mexico and 35% on Canada (tied to drug trafficking concerns), an extra 40% on Brazil (punishing recent unfriendly actions by Brasília), and 25% on India (over its purchase of Russian oil). These tariffs, set to take effect Sept. 8, dramatically escalated trade tensions outside of Europe and sowed uncertainty for multinational businesses. The U.S. also broadened its use of Section 232 tariffs on security grounds, extending 50% metal tariffs to hundreds of steel-containing products. Despite this aggressive stance, markets largely shook off the news, having grown somewhat accustomed to the administration’s trade brinksmanship. In fact, in the case of key allies like the EU and Japan, there was progress: U.S. negotiators reached deals that soften the tariff blow (more on Europe below). Many companies are navigating the new trade landscape by reorganizing supply chains and swallowing some costs. As one macro analyst observed, “we are only seeing limited pass-through from the tariffs” to consumer prices so far. That said, tariffs have clearly dented business confidence in manufacturing and contributed to the slower hiring seen in August[2]. With the Fed likely to cut rates, there’s hope monetary easing will offset some of the trade-related drag on the economy. All eyes will be on the Fed’s meeting and dot-plot projections in the upcoming week to gauge how much policymakers think the tariff turmoil will slow the U.S. outlook – and how far they might go in providing stimulus.

European Union: Trade Truce with U.S. Eases Fears as ECB Holds Fire, Economy Proves Resilient

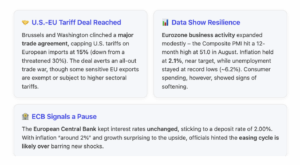

Transatlantic Trade Truce: A potential U.S.–Europe trade war was averted this week thanks to a hard-fought deal between Brussels and the Trump administration. Under an agreement finalized in late August (announced by EU President Ursula von der Leyen and U.S. President Trump), the U.S. will impose a 15% blanket tariff on most European Union goods, far lower than the 30% rate Trump had threatened earlier. In exchange, the EU agreed to eliminate tariffs on U.S. autos and industrial goods entirely, and both sides pledged hundreds of billions in bilateral investments. Some European products will be exempt from the 15% U.S. tariff – notably aircraft, cork, and generic pharmaceuticals are carved out – while a few categories face separate higher tariffs (for example, certain steel-related goods still incur a 50% U.S. tariff, as the U.S. presses its metal trade case). The deal, struck on July 27 and going through legislative approvals in early September, brought a sense of stability and predictability after months of brinkmanship. Von der Leyen noted it’s preferable to the “painful” 27.5% U.S. auto tariff that was in force previously, and EU officials said a 15% tariff is low enough to keep transatlantic trade flowing. European businesses reacted with mixed feelings: relief that a catastrophic trade rupture was avoided, but concern that 15% tariffs still pose a significant cost on exporters. The head of the European Parliament’s trade committee cautioned that many have “doubts about the deal” and suggested it may be amended during the ratification process. Indeed, friction remains – just last week President Trump alarmed EU officials by threatening new tariffs in response to Europe’s digital services taxes, prompting questions about whether the U.S. will stick strictly to the agreement. For now, though, the tariff truce has helped remove a dark cloud from European markets. Automakers like BMW and Volkswagen, which faced the specter of much higher U.S. duties, welcomed the news; their stock prices rose in recent weeks as odds of a deal increased (each climbing roughly 3-5% since late August, according to trading desks). More broadly, the de-escalation with the U.S. – alongside an earlier deal with Japan – means the EU can breathe easier about its export outlook, even as it still contends with other challenges (like slower demand from China). EU Trade Commissioner Sabine Weyand urged the European Parliament to approve the U.S. deal, arguing “you need to look at the alternative” — without it, Europe would be hit by far worse tariffs and uncertainty. The bottom line: the worst-case trade war scenario has been sidestepped, providing a meaningful tailwind for European investor sentiment heading into autumn.

Economic Indicators Improve Slightly: Europe’s economy, which earlier in the year was teetering near recession, delivered some better-than-expected data this week. Most notably, the HCOB Eurozone Composite PMI (Purchasing Managers’ Index) for August came in at 51.0, marking a 12-month high and indicating the fastest expansion in a year[4]. This uptick was driven in part by a surprising rebound in manufacturing – the Eurozone Manufacturing PMI jumped to 50.7 (from 49.8 in July), the first reading above the boom-bust line of 50 in three years[4][4]. Factory output in powerhouse Germany showed signs of stabilization, aided by easing supply strains and perhaps some front-loading of orders before tariffs hit. The services PMI, while slightly lower at 50.5, still signaled modest growth in Europe’s large service sector[4]. These data suggest the Euro-area private sector is managing a “weak expansion”, defying those who predicted a downturn. Meanwhile, inflation in the Eurozone held steady. Preliminary figures showed consumer prices rose about 0.2% in August, putting annual headline inflation at 2.1%[4] – essentially on target for the European Central Bank. Core inflation is a bit higher (~2.4%), but overall price pressures appear stable, with no signs of either deflation or a runaway spike. Unemployment remained at a record-low ~6.2%, as labor markets stay tight (helping support wages and consumption). However, not all indicators were rosy. Retail sales across the 20 euro-area countries fell 0.5% in July from the prior month, a sharper drop than expected[2]. Year-on-year, retail volumes were up 2.2%, but that was slightly below forecasts[2]. The decline was driven by lower sales of food (-1.1%) and fuel (-1.7%), hinting that consumers may be cutting back amid broader economic uncertainties[2]. Analysts noted this slowdown “raised concerns whether robust domestic consumption could continue to buffer the region’s economy against the impact of US tariffs.”[2]. In other words, Europe’s internal demand has been a bulwark against external shocks, but cracks are emerging as people feel the pinch of higher prices and caution creeps in. Still, thanks to decent employment and some fiscal support in countries like Germany, domestic demand remains a relative bright spot. All told, Europe enters September in better shape than many anticipated: GDP is on track for modest growth in Q3 (perhaps ~0.2-0.3%), and the dreaded prolonged recession hasn’t materialized. One headwind has been the strong euro, which climbed to about $1.17 – up in recent months on Europe’s improved outlook – potentially damping export competitiveness. But even that trend showed signs of reversing late in the week, as the dollar regained ground on Fed cut rumors.

ECB Holds Steady, Signals Easing Cycle’s End: Against this backdrop, the European Central Bank took a “wait-and-see” approach, leaving policy unchanged at its (informal) early September deliberations. (The ECB’s next formal meeting is September 10, where it is also widely expected to stand pat.) The ECB’s key deposit rate remains at 2.00%[4] – a level reached after an unprecedented series of eight rate cuts from mid-2024 through mid-2025 that were aimed at countering last year’s slump. With inflation now “around the 2% medium-term target” and the growth outlook slightly better, officials see little urgency for further easing. In fact, ECB President Christine Lagarde struck an upbeat tone in recent remarks, saying “we are still in a good place” economically and noting “inflation is where we want it to be”. Privately, many ECB policymakers believe the easing cycle is done – barring a major new shock like a severe escalation in the trade war or a financial crisis. Market pricing reflects that view: eurozone bond yields have ticked up in anticipation that no more rate cuts are coming. The 2-year German Bund yield is around 1.9%, up from 1.7% a month ago. Money markets are pricing in minimal chance of any additional ECB cut this year. This week Lagarde emphasized a “meeting-by-meeting, data-dependent” stance, giving the ECB flexibility but also reinforcing that “we’re not on a pre-set path.” Economists read that as code for “likely on hold unless things drastically worsen.” Notably, the ECB’s latest staff forecasts (to be published next week) are expected to show inflation hovering ~2.1% in 2025 and growth around 1.2% – projections similar to June’s, and consistent with a stable policy rate. One area of focus is credit conditions: the ECB’s easy money has filtered through, and credit growth in the eurozone has picked up after a drought last year. As long as financial conditions remain supportive, the ECB will feel comfortable pausing. There are, however, risks that could change the script. Officials highlighted “headwinds” like “higher tariffs, a stronger euro, [and] competition” that could hold back growth, as well as the possibility that underlying inflation might ebb more slowly than hoped (wage growth has been strong in some countries). For now, though, the consensus is that the 2% deposit rate is the likely bottom of this cycle. European markets responded positively to the steady hand: the STOXX Europe 600 index ended the week around 555 points, up about +1% and logging its first weekly gain in three weeks (helped by the global rally on Fed expectations). European bank stocks jumped ~4% on the week, rebounding as higher yields promise better profits and as relief over the U.S. trade deal set in. European defense-sector shares even hit record highs (surging 6% this week) amid geopolitical jitters with Russia. The euro, however, eased slightly to ~$1.17 late in the week, as investors acknowledged that while the Fed is likely to cut, the ECB is probably done – a dynamic that could limit further euro appreciation. Overall, Europe heads into the fall with cautious optimism: the trade truce and steady policy form a welcome buffer, even as the region keeps a wary eye on global risks and on whether its nascent recovery can sustain momentum.

Asia: Japan’s Market Hits Multi-Decade Highs Amid Easing Hopes, China Slowdown Spurs Stimulus Talk

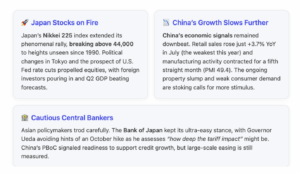

Japan: A Red-Hot Market and Steady Policy – Japanese financial markets were a standout performer this week, as the country’s equities surged on a potent mix of domestic and global drivers. Tokyo’s benchmark Nikkei 225 index pierced the 44,000 mark, setting new multi-decade highs. The broader TOPIX also notched a record, trading near 3,160. By some measures, Japanese stocks are up ~46% from their spring lows. The rally has been fueled by a confluence of factors. One is political change: former Prime Minister Shigeru Ishiba unexpectedly announced his resignation, prompting a leadership contest that investors hope will lead to even more pro-growth policies. The leading contender, Sanae Takaichi, advocates for stronger fiscal stimulus and is resistant to premature rate hikes – music to the ears of a market addicted to easy money. Even her rival offers continuity, so either outcome is seen as market-friendly. At the same time, expectations of global monetary easing (especially a U.S. Fed cut) have boosted risk appetite worldwide, and Japan is no exception. A more dovish Fed tends to weaken the dollar, which this week helped nudge the yen below ¥148 per USD (making Japanese exports more competitive and also encouraging Japanese investors to repatriate into local stocks). Perhaps most importantly, Japan’s own economic fundamentals have impressed. Revised data show Japan’s Q2 GDP grew at a 2.2% annualized rate, more than double expectations. Both domestic spending and exports contributed to growth, defying those who expected the post-COVID rebound to fizzle. Corporate earnings have also been robust: many Japanese firms, from industrials to tech, have beaten profit forecasts and announced shareholder-friendly moves like stock buybacks. Notably, tech investor SoftBank swung back to profit in Q1 (aided by AI investments) and electronics giant Sony raised its annual outlook on strong results – signs that Japan’s tech sector is thriving alongside the U.S. AI boom. Foreign investors have taken notice and are pouring money into Japan. Overseas funds bought an estimated ¥3.5 trillion ($24B) in Japanese equities in August alone, attracted by relatively reasonable valuations and Japan’s status as a “third pillar” of tech investing (offering an alternative to pricey U.S. markets and shaky Chinese tech). Meanwhile, domestic investors are also moving off the sidelines, shifting some of their vast cash holdings into stocks now that inflation (around 3% in Tokyo) is eroding the value of savings. This influx of capital has provided a strong tailwind that “cushions the market against external shocks”.

Amid the stock euphoria, Japan’s central bank remained characteristically cautious. The Bank of Japan (BOJ) did not hold a policy meeting this week, but officials have been telegraphing a steady message: no sudden changes to ultra-loose policy, despite creeping inflation. August data showed Tokyo’s core CPI eased slightly to an annual rate around 2.8–2.9% (down from 3.2% mid-year), suggesting nationwide inflation may also be peaking. That takes some pressure off the BOJ to adjust its yield-curve control or negative interest rate settings. At a speech in Tokyo, BOJ Governor Kazuo Ueda emphasized that tariff uncertainties pose a downside risk, and hinted the bank wants to see how global trade frictions play out before any policy tweak. According to one Reuters summary, Ueda likely “won’t give clear hints on whether the BOJ could hike [rates] in October, as it wants to do more checks on how deep the tariff impact could be.” In plain terms, the BOJ is content to keep its key rate at -0.1% and the 10-year JGB yield pinned near 1.6% for now. With the Fed about to cut and the European Central Bank on hold, Japan sees little urgency to tighten and risk strengthening the yen. Indeed, Japan’s 10-year bond yield has been stable around 1.59%, just below its high for the year. Many analysts think the BOJ might only start very gradually normalizing policy in late 2025 if inflation remains over 2%. For the time being, easy money, strong earnings, and progress on trade (the U.S.-Japan tariff deal signed in July is being implemented, with Washington set to lower auto tariffs by Sept. 16 per that pact) all underpin the positive story for Japanese assets.

China: Slowing Economy Spurs Stimulus Talk – In contrast to Japan’s brightening picture, China’s economy continued to flash warning signs. Fresh data showed that consumer spending and factory output in China are losing steam. In July, retail sales growth cooled to just +3.7% year-on-year, the slowest pace so far in 2025 and well below forecasts of ~5%[4]. This suggests Chinese consumers remain cautious despite summertime promotions and government vouchers. Manufacturing activity shrank for the fifth consecutive month in August, with the official NBS Manufacturing PMI at 49.4 (still under 50, though a hair above July’s 49.3)[4]. Manufacturing has been weighed down by weak global demand and persistent trade uncertainties (not helped by the new U.S. tariffs slated to hit Chinese goods). The services sector in China, which had been a pillar of post-pandemic recovery, also showed signs of plateauing – the services PMI hovered just above 50, barely in expansion territory[4]. Perhaps the most troubling indicator is the property market: the real estate downturn deepened, with real-estate investment plunging 12% year-to-date versus a year ago[4]. This is nearly as severe as the contraction seen during the 2020 COVID shock. Property sales and prices are falling in most cities, undermining consumer wealth and local government finances. Combined, these factors point to an economy that “lacks momentum”, as even officials admit[4][4]. The urban unemployment rate ticked up to 5.3% in August (a 16-month high), and youth unemployment is so troubling that authorities have paused publishing the figure. Facing these headwinds, Chinese policymakers are increasingly expected to unveil new stimulus measures. Last year, a similar summer slowdown prompted the People’s Bank of China (PBoC) to cut rates and spawn a late-year rebound. Will history repeat? Many economists think so. “We expect the recent softening of momentum to strengthen the case for unveiling new stimulus ahead,” wrote ING’s China economics team this week. They noted that a year ago, big policy moves (like infrastructure spending and credit easing) helped China hit its growth target; a comparable push may be needed now. So far, Beijing’s response has been measured: the PBoC has trimmed some key interest rates (most recently in August) and encouraged banks to boost lending, and officials have floated tax breaks for homebuyers and more infrastructure bond issuance. But we have not yet seen a massive “all guns blazing” stimulus. There are signs the government prefers targeted support – for example, some consumer subsidies (such as trade-in rebates for appliances) were implemented over the summer, though their effect appears to be waning. Top leadership has also launched campaigns to shore up business confidence and vowed to tackle local debt risks. The next opportunity for a bigger policy package could be the upcoming October Party plenum or if data for August and September (to be released soon) show further deterioration. Market participants are split: some expect a reserve requirement cut or even an interest rate cut in the coming weeks, while others think Beijing will stick to smaller, “incremental and targeted easing” unless growth falls dangerously short of the 5% annual goal.

Despite China’s issues, Asian markets outside China generally fared well this week, lifted by the positive sentiment from Wall Street and Tokyo. Hong Kong’s Hang Seng Index climbed to around 26,000 (its highest in about 20 months) as investors anticipated possible Chinese stimulus and enjoyed a tech stock bounce. South Korea’s KOSPI rose modestly (~+0.5%), helped by expectations that the Fed’s dovish turn could weaken the dollar and benefit emerging markets. In Seoul, chip giant SK Hynix saw its stock jump on hints of record revenue, echoing the AI chip enthusiasm that lifted U.S. peers. Oil prices remained relatively low – Brent crude traded near $66-68/barrel, and WTI around $62[1] – which is a positive for oil-importing Asian economies (and also a sign that global demand concerns persist). In currency moves, the Chinese yuan held around 7.26 per dollar; traders suspect the PBoC is quietly supporting the yuan to prevent excessive weakening, which would complicate the inflation picture. The Indian rupee and other Asian currencies strengthened slightly against the greenback on the week’s global risk-on mood.

Looking Ahead: The first week of September showcased a world economy at an inflection point – cooling enough to prompt central banks to pivot toward stimulus, but not so cold as to stall corporate profits or spur financial panic. Global markets largely reacted with optimism, pricing in the “sweet spot” of easier monetary policy ahead. However, significant challenges loom: trade conflicts remain a wild card (as evidenced by Trump’s latest tariff salvos), China’s slowdown could deepen if policy support disappoints, and even in the U.S., the question is whether the Fed can engineer a gentle landing or if the rising jobless rate foreshadows a sharper downturn. For now, investors are focusing on the positives: the Fed is expected to cut rates on Sept. 17 (with possibly more to follow by year-end), the ECB seems confident in Europe’s trajectory, and Asian policymakers are keeping conditions accommodative. As one Morgan Stanley economist summed up the Fed’s stance, “ignore where inflation is today and ease policy to support the labor market” – a mantra that could well describe the broader global policy environment. That prescription is boosting market sentiment now, but the coming weeks will test whether reality lives up to the hopeful narrative. In the meantime, the headlines from Aug 31–Sep 6 leave us with a cautiously encouraging picture: rate cuts are on the horizon, trade peace is (partially) restored, and while growth is uneven, a coordinated downturn has been kept at bay – for the moment.

References