Global Markets Rally on Tech Earnings and Trade Deal Hopes

The Vortex – Global Market Weekly – 20–26 July, 2025

Summary: Global economic and financial news for the week of July 20–26 was dominated by surging stock markets and major policy developments across regions. In the United States, equities hit record highs as a robust earnings season – led by big tech – fueled optimism, while the Federal Reserve stayed on a steady course. In the European Union, the ECB held interest rates unchanged amid improving economic indicators and looming U.S. trade tariffs. Across Asia, a landmark U.S.-Japan trade deal and resilient corporate results lifted markets, even as policymakers kept an eye on inflation and growth signals. Below is a regional breakdown of the week’s biggest global finance headlines, complete with key data, expert insights, and embedded charts for context.

United States: Wall Street Hits Highs as Earnings Impress and Fed Stands Pat

United States: Wall Street Hits Highs as Earnings Impress and Fed Stands Pat

Stocks Surge to Records: U.S. equity markets extended their rally through late July, breaking record levels despite various macro uncertainties. The S\&P 500 closed above the 6,300 mark for the first time on Monday and kept climbing to finish the week at 6,388.64[1][2]. That marked the index’s fifth consecutive record close and about an 8% gain year-to-date[3]. The tech-heavy Nasdaq Composite similarly notched all-time highs, ending around 21,108[2]. Mega-cap technology stocks – sometimes dubbed the “Magnificent Seven” – propelled these gains, reflecting investor confidence in sectors like cloud computing and AI. For instance, shares of Meta and Amazon rose over 1% on the week[4][5]. Even recently volatile “meme” stocks saw a revival; real-estate platform Opendoor Technologies skyrocketed amid retail trading fervor (at one point up 120% intraday)[6][7]. These broad advances pushed the Dow Jones Industrial Average within a hair’s breadth of its record – the Dow surged to 45,010.29 mid-week, just shy of its all-time high close[3]. By Friday, the Dow settled near 44,900, capping a weekly gain of ~1%[2]. Market volatility remained subdued throughout, with the VIX “fear index” dipping to five-month lows[3] – a sign of growing investor calm as indices climbed.

Blockbuster Earnings Boost Confidence: A strong Q2 earnings season underpinned U.S. market optimism. With roughly one-fifth of S\&P 500 companies reporting by mid-week, over 85% topped profit expectations, according to FactSet[4]. Earnings are on track to rise around 5% year-on-year in Q2, a sharp improvement from prior quarters[4]. Technology giants were in focus with mixed results: Alphabet (Google) delivered a standout report, exceeding revenue ($96.4 B vs. ~$94 B expected) and EPS ($2.31 vs $2.18) estimates[8]. Google’s ad and cloud businesses both outperformed, and management boosted 2025 capital spending plans by $10 B, citing “strong and growing demand” for AI-driven cloud services[6][8]. This news sent Alphabet shares up ~3%[5] and lifted sentiment across tech. In contrast, Tesla reported softer results: Q2 revenue of $22.5 B slightly missed forecasts and was down 12% from a year earlier[6]. The electric automaker’s deliveries lagged, and CEO Elon Musk cautioned that the company “probably could have a few rough quarters” ahead due to higher costs and waning EV subsidies[6]. Tesla’s stock dipped on the outlook. Outside of tech, an industrial standout was GE Vernova – the newly formed power and renewable energy unit of GE – which saw its stock jump 14.6% to a record high after smashing profit forecasts and raising cash flow projections[3]. Meanwhile, chipmaker Texas Instruments offered a note of caution, slumping 13% after warning of weaker demand for its semiconductors amid tariff uncertainties[3]. Overall, however, investors viewed the earnings momentum positively, with one strategist noting that with expectations so low, “the end result will be better than anticipated” – an encouraging sign for the market’s trajectory[4].

Fed Holds Fire Amid Mixed Data: U.S. central bank policy took a backseat as the Federal Reserve’s next meeting loomed just beyond the week. The consensus on Wall Street was that the Fed would keep its benchmark rate unchanged for a fifth straight meeting, maintaining the federal funds rate in a 4.25%–4.50% range established earlier in the year[6]. Solid economic data gave the Fed room to stand pat. Notably, the labor market remained resilient – June nonfarm payrolls rose by 235,000 and unemployment held at 3.7%[6] – supporting the Fed’s view that no immediate cut was needed. Inflation appeared contained enough that new tariffs (more on that below) had yet to notably lift prices[4]. During the week, fresh figures showed existing home sales fell more than expected in June, hinting at pockets of cooling in interest-sensitive sectors[3]. But other indicators were bullish: S\&P Global’s flash PMI for U.S. composite output jumped to 54.6 in July (from 52.9 in June), the fastest expansion this year, led by booming services activity[9][9]. This mix of strong employment and decent growth has traders ruling out a July rate cut – futures put near-zero odds on it[3]. Attention is turning to whether the Fed might ease later in the year; as of this week, markets saw only a roughly 58% chance of a September cut[3]. Fed Chair Jerome Powell, while not speaking publicly this week, has emphasized data-dependence. (It’s worth noting the White House’s unusual pressure on the Fed: President Donald Trump met with Powell at Fed headquarters on Thursday in a rare visit[10], after repeatedly urging rate reductions. However, Fed officials have maintained their independence, and no policy change resulted from the encounter.) Overall, the Fed’s “higher for longer” stance stayed intact – a point reinforced by a six-week low in weekly jobless claims (217,000, better than expected)[9], suggesting the economy could handle steady rates.

Trade and Tariffs in Focus: U.S. markets also navigated developments in international trade policy, a key overhang on sentiment. Over the weekend, Commerce Secretary Howard Lutnick reiterated an August 1 deadline for America’s trading partners to come to tariff agreements, calling it a “hard deadline” for new levies to kick in[4]. This raised the stakes for talks with the EU, China, and others. Investors, however, grew more optimistic that deals would be struck in time. Indeed, by mid-week, reports surfaced of a breakthrough with the EU – an emerging U.S.–EU trade deal that would impose a flat 15% tariff on European imports, mirroring a pact just reached with Japan[3]. Washington sent formal letters to dozens of countries detailing tariff plans of 20%–50% if negotiations failed[5]. But the “confidence that the White House will work through these trade deals” helped boost risk appetite[3]. Reflecting trade hopes and strong earnings, the U.S. dollar index (DXY) fell to around 97.8, a one-month low, easing financial conditions[5]. Gold prices, often a haven, hovered near $3,370/oz after a modest weekly rise[9], as traders wagered that any tariff-induced inflation might be met with a measured Fed response. All told, U.S. financial markets ended the week in a position of strength, riding a wave of earnings optimism and guarded confidence that trade spats and Fed decisions would not derail the economic expansion.

European Union: ECB Pauses Easing as Economy Proves Resilient, While Trade Tensions Simmer

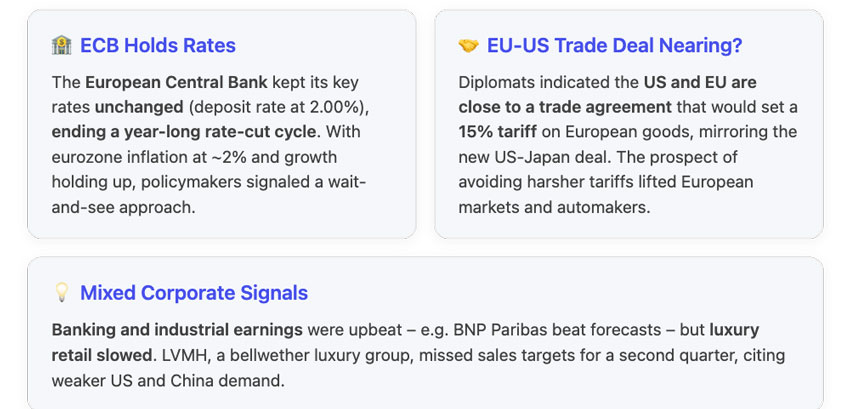

Central Bank Stands Still: The European Central Bank (ECB) took center stage in Europe this week, as it held a policy meeting on July 25. In line with expectations, the ECB left interest rates unchanged, maintaining its deposit facility rate at 2.00% and main refinancing rate at 2.15%[6]. This decision formally paused the ECB’s easing cycle after eight consecutive rate cuts over the past year[6]. ECB President Christine Lagarde struck a cautiously optimistic tone. She noted the eurozone is “in a good place” economically[9] – inflation has eased to the 2% target as of June, and growth earlier in 2025 exceeded expectations[9][9]. Indeed, recent data showed Eurozone unemployment at record lows (~6.2%) and business surveys improving, signs that the economy is holding its own despite external headwinds. Given this backdrop, Lagarde and colleagues saw no urgent need for further rate cuts. However, they emphasized “monitoring” developments, especially regarding global trade disputes and the stronger euro. (Notably, euro strength has been a byproduct of the region’s resilience – the euro traded around $1.17, up in recent weeks[9], which makes European exports relatively pricier abroad.) The ECB also released updated staff forecasts indicating inflation hovering near 2% over the next year and growth slowing modestly, scenarios that justify a prolonged rate pause. Investors reacted by dialing back expectations of more ECB stimulus in the near term. Yields on European bonds actually rose after the meeting, as markets priced out chances of a September rate cut following Lagarde’s suggestion that additional easing “might not be needed” if conditions hold[9][9]. The two-year German bond yield spiked to a two-month high (~1.92%) on this hawkish interpretation[9]. In sum, the ECB communicated a wait-and-see stance – ready to resume cutting if the economy falters, but content for now that policy is “mildly accommodative” at current levels[11][11].

Equities Edge Up, Trade Concerns Linger: European stock markets climbed modestly during the week, supported by the global rally and relief over the ECB’s steady hand. The STOXX Europe 600 index ended around 552 points, rising roughly +0.3% on Thursday alone after the ECB decision[9]. That put the STOXX 600 near its highest level in over a year. Similarly, the Euro STOXX 50 (blue-chip eurozone stocks) hit ~5,360[9], with strength in industrials and financials offsetting softness in luxury goods. European investors were encouraged that a feared U.S.–EU trade war might be averted. By mid-week, multiple reports suggested that Washington and Brussels were close to a trade agreement to resolve tariff disputes[3]. The outlines of the potential deal include a 15% across-the-board tariff on EU exports to the U.S. – a compromise measure that, while significant, would avoid the even steeper duties that the U.S. had threatened (some as high as 25–50% on certain goods)[5][7]. This mirrored the tariff terms the U.S. set with Japan days earlier. Signs of progress on U.S.-EU trade lifted Europe’s auto sector in particular, as carmakers would escape worst-case tariffs. Shares of Volkswagen, BMW, and Renault ticked higher on the news (each up ~1–2% mid-week, per traders) as tariff clouds began to part. Still, uncertainty hasn’t completely vanished – EU officials cautioned that if talks failed by the Aug. 1 deadline, Europe is prepared to retaliate with tariffs on €93 billion of U.S. goods[9]. This kept some investors on edge. The euro’s slight weakening later in the week (to ~$1.175) hinted at caution as the deadline approached[9]. For now, though, the mood in European markets was broadly positive, supported by both global cues and local developments.

Corporate Highlights – Banks Up, Luxury Down: European corporate earnings and news yielded a mixed bag of signals. On the positive side, banking and industrial firms showed strength. France’s largest bank BNP Paribas reported better-than-expected revenues and earnings for Q2, citing solid trading results and lending volumes. BNP’s stock rose about 0.4% Thursday following the beat[9]. Other eurozone banks also outperformed this week, continuing a trend of European bank stocks outpacing U.S. peers in 2025. In manufacturing, some indicators were upbeat – Germany’s Ifo business climate index came in slightly above forecasts, suggesting business sentiment stabilizing despite export worries (this was reflected in a modest rise in the DAX index). However, Europe’s consumer-facing sectors flashed warnings. LVMH, the world’s largest luxury goods conglomerate and a bellwether for high-end spending, reported a sharp drop in sales in its key Fashion & Leather division. Organic sales in that segment fell 9% in Q2, worse than expected, as affluent shoppers in the U.S. and China pulled back[12][12]. This was LVMH’s second consecutive quarterly miss, sparking concerns of a broader luxury slowdown. The company’s shares fell ~2% on the results, and have slid about 28% over the past year[12][12]. LVMH’s management cited economic uncertainty, trade tensions, and weaker consumer confidence, particularly among wealthy clients, for the downturn[12][12]. On the bright side, LVMH noted signs of life in Europe and Japan’s luxury markets (helped by tourism), and expressed “cautious optimism” that progress on EU-US trade talks (i.e. removing tariff threats) could improve the “mood” for luxury buyers going forward[12]. Aside from luxury, energy markets in Europe saw some volatility: oil prices steadied around $66–69/bbl for Brent crude[9] after posting their strongest weekly gain in months, partly on hopes that improved U.S.-China trade dialogue would boost demand. Natural gas prices in Europe remained relatively low, easing pressure on manufacturers.

Outlook: As July drew to a close, Europe’s economy appeared to be navigating between global crosscurrents relatively well. The stabilization of inflation at target is a major relief for the ECB, allowing policymakers to shift from emergency easing to observation mode. However, challenges remain – notably, the full impact of the U.S. tariffs (even at 15%) has yet to be seen on Europe’s export-driven industries. The ECB’s top economist Isabel Schnabel cautioned that trade tariffs “are on net inflationary” and could raise costs over time[11][11], a factor that might complicate policy if inflation sparks up again. For now, though, businesses and investors in Europe seem hopeful that the groundwork of a trade truce is being laid. This optimism, combined with strong bank balance sheets and still-healthy domestic demand, put Europe on slightly firmer footing heading into August.

Asia: Trade Agreement Spurs Market Rally as Japan Leads Gains, While Growth Signals are Mixed

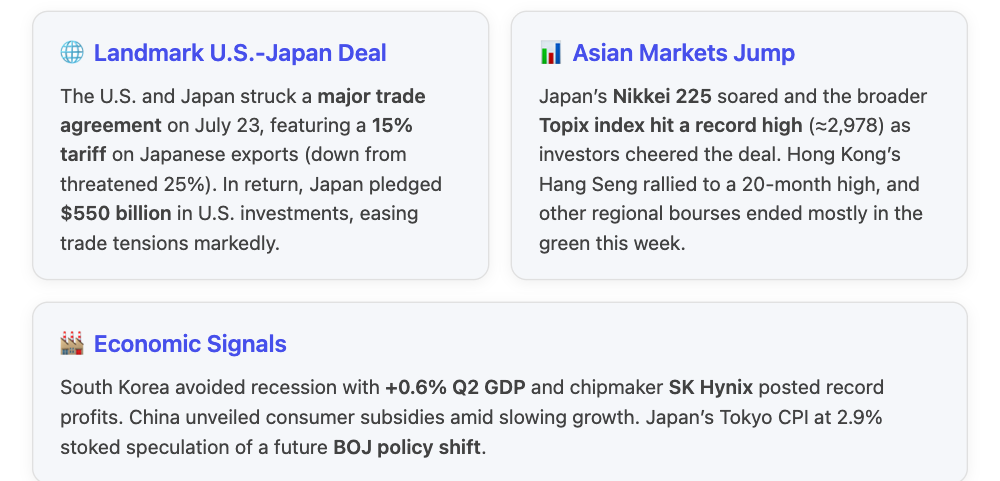

Trade Breakthrough Boosts Japan: The big news in Asia was the United States and Japan sealing a landmark trade deal, which was announced on July 23. After months of negotiation, President Trump and Japan’s Prime Minister (Shigeru) Ishiba agreed on a pact that imposes a 15% tariff on Japanese exports to the U.S. – a lower rate than initially feared – in exchange for significant Japanese investments and market concessions[7][7]. This “United States–Japan Trade Agreement” represented a compromise: the U.S. had previously threatened tariffs up to 25% on autos and other goods, which would have hit Japan’s economy hard[7]. Under the deal, Japan avoids those higher duties; in return, it committed to investing $550 billion in U.S. projects (in infrastructure, energy, technology, etc.) and to increase imports of American agricultural products[7]. The agreement also maintains steep 50% U.S. tariffs on Japanese steel/aluminum, but overall was seen as diffusing a major trade dispute[7]. Financial markets across Asia roared approval. In Tokyo, the benchmark Nikkei 225 index jumped over 3% following the news[7], and by Thursday it closed at 41,826.34, near its highest level ever[10]. The Topix, a broader index, rallied 1.75% to a record high ~2,977.5[10]. Major Japanese multinationals surged: Toyota shares, for example, spiked as much as +14% over the week[7], reflecting relief that auto tariffs would be capped at 15%. Investors also cheered Japan’s guaranteed access to the U.S. market for critical exports like cars and electronics. The trade deal was described by analysts as “historic” and a potential template for U.S. agreements with other nations. Coinciding with the deal, the White House hinted at progress in talks with South Korea and the EU on similar terms. Negotiators from the U.S. and China were also set to meet in Stockholm, suggesting a broader thaw in trade tensions[9]. This backdrop of easing trade uncertainty provided a powerful tailwind for Asian equities throughout the week.

Asian Markets Mostly Higher: Beyond Japan, equity markets in the Asia-Pacific region largely traded in the green. Hong Kong’s Hang Seng Index rose for five sessions straight, reaching about 25,667 on Thursday – its highest level since November 2021[9]. Hong Kong stocks were buoyed by global trade optimism and expectations of Chinese policy support. In mainland China, the CSI 300 index of Shanghai/Shenzhen stocks climbed ~0.7% Thursday[10], and was up about 4% for the month of July amid hopes that authorities would stimulate the economy. South Korea’s KOSPI gained modestly (+0.2% on Thursday) to around 3,190 points[10], and Seoul’s tech-heavy KOSDAQ was roughly flat after an earlier rally. Australia’s ASX 200 was one outlier, ticking down ~0.3% as weak commodity prices weighed on mining shares[10]. Overall, MSCI’s broad Asia-Pacific index hit its best level in about 18 months. Asian currencies saw some action too: the Japanese yen initially strengthened on the trade deal news (as capital flow concerns eased), with USD/JPY dipping to the mid-147 range[9]. Meanwhile, the Chinese yuan appreciated to its strongest value against the dollar since late 2024 (around CNY 7.14 per USD)[10], reflecting both a weaker dollar globally and anticipation of Chinese economic support. By week’s end, the U.S. dollar regained a bit of ground against Asian currencies as traders repositioned ahead of the Fed and Bank of Japan meetings.

Economic & Policy Signals: Asia’s economic data out this week painted a mixed picture. Japan’s inflation showed persistence: Tokyo’s core consumer price index (a leading indicator) rose 2.9% in July from a year earlier[9]. This beat expectations and stayed above the Bank of Japan’s 2% target, fueling speculation that the BOJ might adjust its ultra-easy policy soon. Indeed, investors are looking to next week’s BOJ meeting for a possible upward revision to inflation forecasts[9] or tweaks to its yield curve control program. Japanese government bond yields ticked up in response. However, BOJ officials have signaled caution, given that parts of Japan’s economy (e.g. exports) have been hurt by U.S. tariffs and an earlier global slowdown[9]. Over in South Korea, there was a notable bright spot: Q2 GDP grew +0.6% quarter-on-quarter, beating forecasts and meaning Korea avoided a technical recession[10]. Strong domestic consumption (+0.7% QoQ) helped offset trade challenges, and GDP was up +0.5% year-on-year[10]. This positive surprise comes after a small contraction in Q1, suggesting Asia’s fourth-largest economy is stabilizing. Another highlight was SK Hynix, the Korean semiconductor firm, which posted record-high quarterly revenue and profit – revenue jumped 35% YoY and operating profit 69% YoY in Q2[10], smashing estimates. Hynix credited booming demand for memory chips used in AI data centers, and its stock leapt ~2.6% on the news[10]. This contrasts with some chip peers like Samsung (which, ahead of its results, warned of a profit slump due to legacy chip oversupply). In China, the world’s second-largest economy, the data was more lukewarm. No major GDP figures came this week (China’s Q2 GDP was released earlier in July at +6.3% YoY, below expectations), but there were signs of Beijing stepping up support measures. Notably, China’s government announced plans to issue subsidy vouchers for senior citizens to encourage spending on elder care and services[10] – a targeted fiscal stimulus aimed at both helping an aging population and boosting domestic consumption. This is a rare direct subsidy move by Chinese policymakers, who generally rely on infrastructure spending or credit easing. The markets read it as a signal that Beijing is concerned about slowing growth and willing to take action. Chinese officials also hinted at potential policy rate cuts or looser property curbs in coming weeks, which helped lift Chinese stocks. Investors are awaiting China’s industrial profit data (due over the weekend) for clues on whether the manufacturing slump has bottomed out[9].

Looking Ahead in Asia: The confluence of a major trade victory for Japan, early signs of tech-sector strength (AI chip demand), and ongoing policy support in China gave Asia a generally positive momentum this week. Market analysts noted that trade-dependent Asian economies have been under great risk from U.S. tariff moves, so the U.S.-Japan deal and progress with other partners is “hugely relief-inducing.” Japan’s exporters now have clarity, and South Korea and Taiwan may be next to secure agreements with the U.S. (though those deals are still in discussion). The Bank of Japan will be in focus next: with inflation running above target and the Fed on hold, some expect the BOJ to tweak its policy – for instance, by allowing Japanese 10-year bond yields to rise a bit more. However, BOJ Governor Kazuo Ueda is likely to move cautiously to avoid choking off economic recovery. For China, the key will be whether stimulus measures can reignite confidence in the second half of the year. If Beijing accelerates spending or eases monetary policy (which could happen as soon as August), it would further bolster regional growth prospects.

In summary, the week of July 20–26 featured broad-based optimism across global markets: U.S. stocks soared on earnings and benign Fed signals, Europe navigated policy and trade challenges with resilience, and Asia saw tangible benefits from de-escalating trade tensions. While risks from tariffs, inflation, and geopolitics haven’t vanished, investors closed out the week in a bullish mood, encouraged by the “goldilocks” mix of good news – strong profits, stable rates, and improving international cooperation – in this mid-summer period.

References

- [1] Sandp 500 Chart By July 2025 | StatMuse Money

- [2] Dow Jones Industrial – Nasdaq Composite – S&P 500 July 2025

- [3] S&P 500 and Nasdaq Rally to Record Highs on Optimism About Trade Deals

- [4] Stock market news for July 21, 2025 – CNBC

- [5] Markets News, July 21, 2025: S&P 500, Nasdaq Close at … – Investopedia

- [6] Markets Break Records: July 21–25, 2025 Weekly Recap

- [7] Weekly Summary 24 July 2025: Tariffs, BBVA & More | Plus500

- [8] Chart of the day – US500 (24.07.2025) | XTB

- [9] Global Market Quick Take: Asia – July 25, 2025 | Saxo

- [10] Asia stock market live updates: U.S.-Japan trade deal – CNBC

- [11] ECB’s Schnabel calls for steady rates as economy holds up in face of …

- [12] LVMH hit by sharp drop in fashion sales as wealthy consumers rein in …